How a once predictable industry became one of Australia’s most strategically contested consumer goods battlegrounds. By 2024-25 the manufacturing landscape crystallised into a contest between three dominant producers. Report for TWM by Tim Woods, Managing Director, IndustryEdge.

Walk down any supermarket aisle and the tissue section looks like a sea of softness – Quilton’s purple packs, Kleenex’s pastel tones, Sorbent’s crisp whites. But behind the branding lies one of Australia’s most quietly intense manufacturing rivalries. Over the last six decades, the Australian tissue market has transformed from a tidy, duopoly style landscape into a fierce tri-cornered contest shaped by global players, nimble local disruptors, sharp-edged import economics and relentless capacity reshuffling.

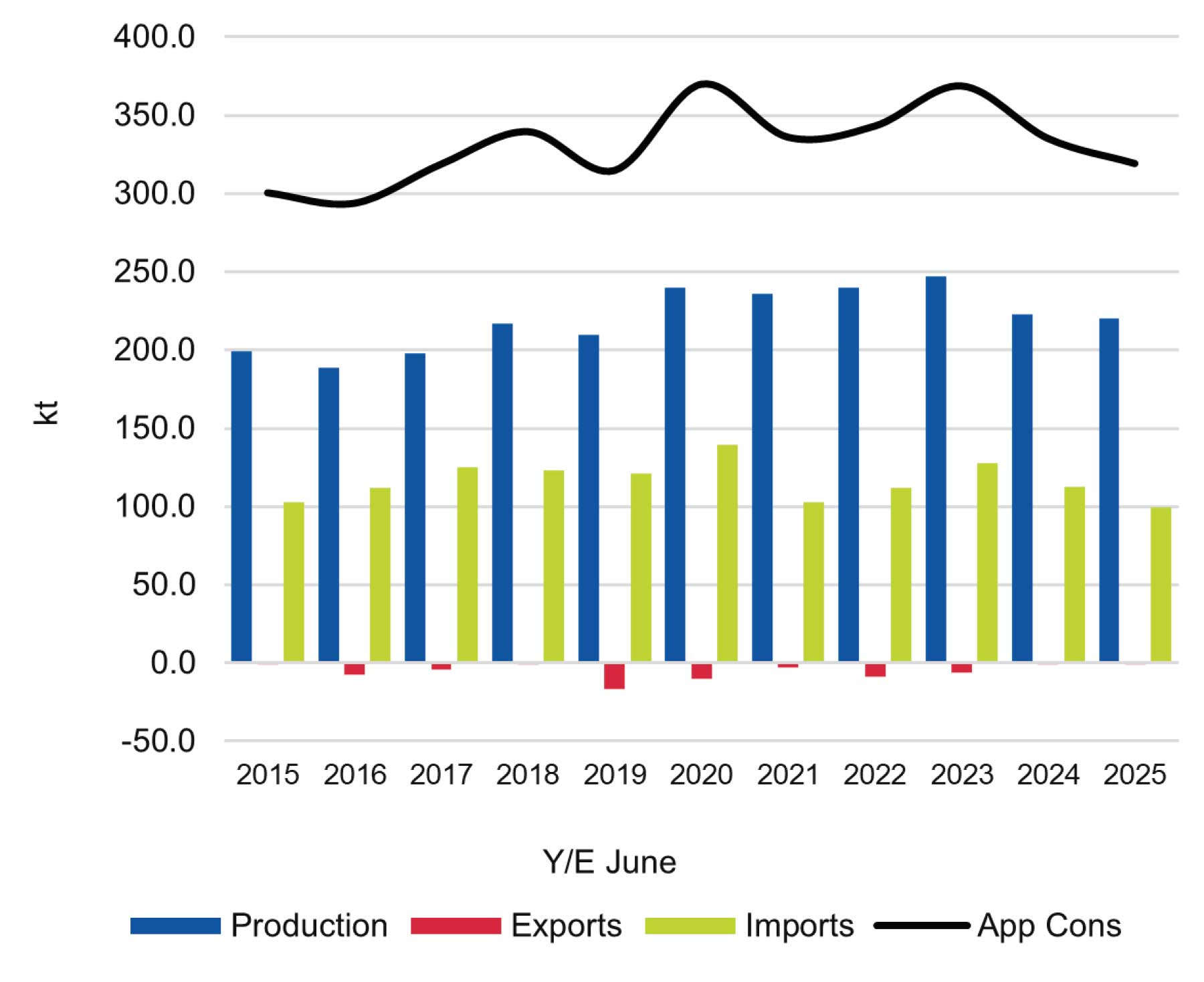

Today, the stakes are higher than ever. Local manufacturing capacity sits at 252,000tpy, utilisation remains high, and imports – both of tissue stock and fully converted products – continue to redefine competitive strategy.

This is the story of how Australia got to this point and where its tissue wars are heading next.

The early years: foundations of a domestic industry

The Australian tissue industry began on steady, traditional footing: a joint venture between APM (later Amcor) and American giant Kimberly-Clark. Kimberly-Clark Australia (KCA) ultimately took full ownership of the Millicent mill in South Australia, a site that still anchors its Australian production today.

By the late 1960s, a second major node emerged – the Box Hill mill in Victoria, created by Bowater Scott. This site later became part of Carter Holt Harvey, forming a Trans-Tasman tissue operation that Essity (then SCA) acquired in 2004.

But it wasn’t the majors who would shake things up next – it was the small players.

The rise of the disruptors

In 1984, Cosco opened a Brisbane tissue mill, followed by the Paper Converting Company (later Merino). Their presence laid the groundwork for what would become the most significant competitive disruption in the industry’s modern history: ABC Tissue.

Initially a converter, ABC purchased Cosco and embarked on an aggressive expansion strategy, including a 30,000tpy machine at Wetherill Park in Sydney. The company quickly grew market share by offering premium quality at lower prices – a one-two punch that reshaped consumer expectations and retail negotiations alike.

By the mid-2000s, ABC Tissue was no longer a challenger brand. It was a genuine heavyweight, aggressively investing in capacity while nimbly leveraging imports of pulp, tissue stock and finished products.

*In the above table of apparent consumption of tissue stock, export figures include stock that has been manufactured in Australia and in some cases converted to tissue products before shipment.

The big three emerge as corporate chess moves dominate

By 2024-25, the Australian tissue manufacturing landscape had crystallised into a contest between three dominant producers:

- ABC Tissue – 100,000tpy (40%)

- Kimberly-Clark Australia – 90,000tpy (36%)

- The Sorbent Paper Company – 32,000tpy (13%)

- Encore Tissue rounds out local capacity with around 30,000tpy.

The competitive tension between ABC, KCA and Sorbent has shaped every strategic decision over the past decade – from machine closures to capacity expansions to import strategies. The last 10 years have been a seesaw of change.

ABC Tissue launched multiple new machines between 2014 and 2020, including replacing the original Brisbane machine and planning another at an undisclosed site. In 2022 it boosted capacity by another 10,000tpy.

KCA retired PM1 and PM3 in 2011–12 and shut the Tantanoola Pulp Mill, reducing capacity by 35,000tpy and focusing on running PM5 – its modern 50,000tpy machine – at close to full utilisation year-round.

Essity divested a 50% stake to Pacific Equity Partners in 2010 to create Asaleo Care. In 2018, APP (Asia Pulp & Paper) acquired its Australian consumer tissue business, rebranding it as the Sorbent Paper Company and injecting new strategic options, especially via its massive Asian manufacturing footprint.

By 2021, Essity reacquired the remainder of Asaleo Care, folding it back into global operations. Then in 2023, Sorbent shut its PM3 machine at Box Hill, tightening domestic supply and increasing import reliance.

Capacity utilisation: the new ceiling

For most of the past five years, utilisation has hovered between 87–88% – historically a trigger point for capacity expansion.

But not anymore.

Imports have broken that old relationship. The economics now make new local machines difficult to justify unless they beat Asia’s enormous cost advantages – an unlikely outcome for a high labour and high energy cost market like Australia.

Recent moves illustrate this perfectly: ABC’s 10,000tpy expansion was immediately soaked up, keeping utilisation steady; Sorbent’s PM3 closure similarly left utilisation unchanged, as imports rose to compensate.

Production and consumption trends: a market redrawn

Domestic production fell to 220,000 tons in 2024 25 – its lowest in years. Apparent consumption also dropped 4.8% to 319,000 tons, the weakest in nine years.

For the first time since the early 2010s, imports of fully converted products – not tissue stock – are driving shifts in supply. ABC, Encore, and KCA remain at or near full capacity, with Sorbent’s remaining TAD machine also running heavily after the PM3 closure.

The import wave: from supporting role to market engine

The biggest transformation of the last decade has been the rise of imports – not just of tissue stock, but of fully converted products.

Tissue stock imports

In 2024-25, tissue stock imports fell to 99,000 tons, their lowest level in 18 years. China remains dominant with a 67% volume share, followed by Indonesia at 27%.

Import prices softened by 3.1%, reinforcing the logic of a flexible “manufacture locally / convert locally / import at will” model used by ABC and Sorbent.

Converted tissue imports

In 2024-25, the value of fully converted imports hit AUD423m, a record. Total tissue related imports reached AUD1.165bn. Growth is strongest in:

- Toilet paper

- Facial tissues

- Sanitary and baby-related categories

Imported product is increasingly shaping retail price points and pressuring domestic utilisation.

Conversion Market Shares: ABC Leads the Pack

When looking specifically at conversion of locally produced tissue stock, IndustryEdge estimates the market is divided as follows:

- ABC Tissue – 41%

- Kimberly-Clark – 32.5%

- Sorbent – 15.5%

- Encore – 11%

ABC’s leadership in both converting and importing gives it unmatched supply flexibility.

Strategic dynamics: the three-way chess match

The current market is best understood as a strategic triangle.

ABC excels at cost competitive manufacturing while also being the biggest importer of tissue stock – allowing rapid volume scaling.

Kleenex and Cottonelle give KCA category strength, but its manufacturing strategy is less flexible than the others.

Backed by APP, Sorbent has unmatched access to low-cost Asian capacity and can shift between domestic manufacture, conversion and direct imports depending on market conditions.

The road ahead: stability through change

With high utilisation, tightening capacity, rising imports and no expansions planned, the next decade of the Australian tissue market will be shaped not by who builds the next machine – but by who best manages flexibility, cost exposure, brand power and supply chains.

Tissue may be soft, but the market competition in Australia has never been harder.