AFRY Management Consulting’s Senior Principal Sanna Sosa, left, reports for TWM with colleagues Soile Kilpi, Director, Management Consulting, and Martin Pereira, Vice President, Sales & Innovation, as the industry swings back towards hard-line market realities.

The North American tissue sector has entered a period of sharper strategic focus. Demand remains resilient, private label continues to gain share, and premium product expectations show no signs of easing. Yet beneath this steady surface, the logic behind capital investment, manufacturing technology choices and sustainability priorities is evolving – shaped by inflationary pressures, regional policy shifts and the growing role of digitalisation.

In a wide-ranging conversation, Martin Pereira offers a candid and experience-based view of how tissue producers are thinking today – about capital allocation, technology choices and the long-term resilience of their assets. Complemented by reflections from Soile Kilpi, discussion provides a 360-degree perspective on a sector balancing short term economics with long term structural shifts.

From sustainability-led growth to cost driven decisions

Over the past decade, sustainability and energy efficiency were central pillars of tissue industry investment strategies. In North America, that emphasis has not disappeared – but it has clearly softened.

“In the US, the focus on energy efficiency and sustainability hasn’t been shelved,” Pereira says, “but it is not as prioritised as it was.” Instead, manufacturers are placing greater weight on manufacturing efficiency, cost reduction and margin protection. The more transformative decarbonisation solutions such as biomass gasification have slowed. “Where I thought we would see more demand on gasification… I’m not seeing that right now,” he adds.

This shift reflects a more pragmatic investment environment. While environmental performance remains important, today’s capital decisions are increasingly driven by economics, customer demand and competitive positioning. Pereira is careful to note that this trend is not universal: “That focus is somewhat different depending on the region today.”

Europe, for example, continues to prioritise sustainability, fibre optimisation and energy efficiency, while North America has become more selective – allowing market realities to take the lead. Cost competitiveness now sits squarely at the centre of decision-making. Energy efficiency measures such as improved hoods, heat recovery and vacuum system optimisation are pursued primarily because they reduce operating expense, not solely to meet decarbonisation targets.

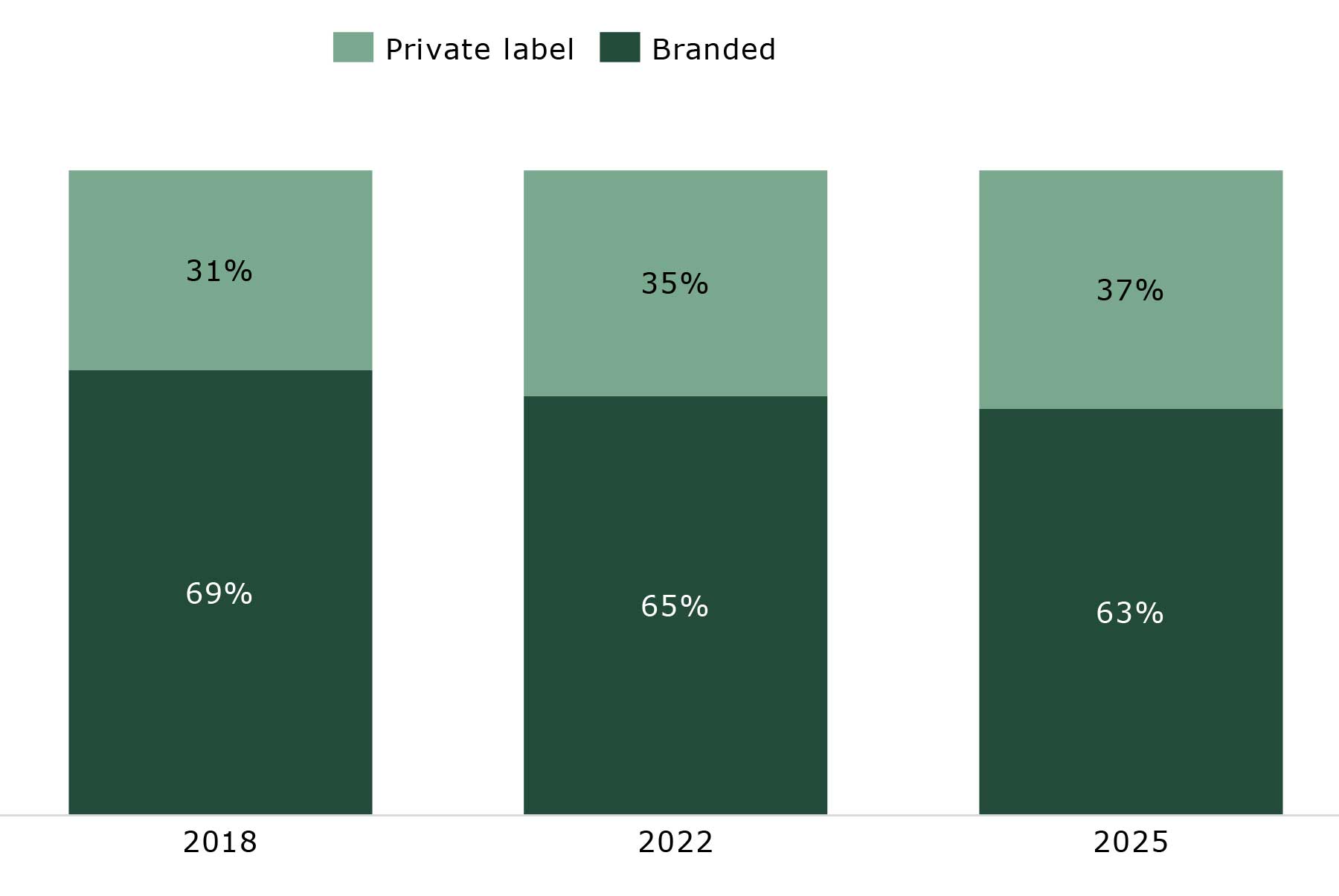

Private label: the engine behind North American growth

Few factors have reshaped the North American tissue landscape as profoundly as the rise of private label. Once positioned as a lower quality alternative, private label tissue has evolved into a growth engine that is driving both capacity additions and technology choices.

“The private label sector in America is driving growth,” says Pereira. “Based on our estimates, it already represents around 37% of the market today and continues to grow.”

This demand is translating directly into investment decisions. Rather than incremental upgrades, many producers are pursuing new, high-efficiency machines that are often dedicated to private label production.

“We’re seeing projects with one machine and three or four converting lines going in now,” Pereira says. “But the plan is to have at least another machine – if not two – added.” In other words, mills are being designed as expandable platforms. The footprint often anticipates a five-year plus growth horizon, even if market conditions ultimately dictate the pace. Kilpi highlights how far private label has come: “In the old days, private label was relatively low quality. Over the past 10 – 15 years, that has completely changed.” Today, private label products often match or even exceed branded offerings in softness, performance and consistency.

New machines over legacy assets

Despite continued investment, North American producers are increasingly selective about where capital is deployed. Large, established players are focused less on expansion and more on asset optimisation and protecting their existing market positions.

“Some of the largest players are trying to protect their markets and margins,” Pereira says. “We are helping them decide whether it’s best to upgrade those assets or build one new machine to replace old assets.”

This approach reflects rising capital costs and a desire to avoid spreading investment too thinly across ageing infrastructure. The profitability gap between modern, energy-optimised machines and older assets continues to widen. For producers operating outside the top cost quartile, strategic decisions cannot be postponed indefinitely.

Faster projects, sharper higher costs

One of the most notable changes is the speed at which projects can now be executed. For greenfield developments, a new tissue machine can be designed, built and started up in as little as 20–21 months.

“It is definitely quicker,” says Pereira. “Today, engineering and construction are done in parallel.”

However, the critical path has shifted: “The largest time component is no longer the machine itself, but the electrical aspects of the project,” he adds, pointing to energy availability and infrastructure as emerging bottlenecks.

Capital expenditure has escalated dramatically since the pre-pandemic period. Inflation, supply chain volatility and especially labour costs have fundamentally reset project economics. In North America, Pereira estimates that new tissue machine investments can be roughly 50% more expensive than they were six years ago. As a result, modularisation strategies and design efficiencies are becoming central to feasibility studies.

By contrast, China has experienced a far more moderate cost increase at around 20% over the same period, largely due to the use of domestic technology and lower construction costs. The gap highlights a growing competitiveness challenge for Western producers.

Technology: incremental hardware, disruptive digitalisation

While core machine concepts remain stable, incremental innovations are meaningful. Shoe press technologies, improved hoods and enhanced heat recovery systems can significantly reduce steam consumption.

“As soon as you increase the dryness of the sheet going to the Yankee, you save energy,” Pereira says. Even small percentage-point improvements translate into substantial efficiency gains.

Producers are also focused on achieving “higher bulk and lower basis weight,” reducing fibre usage, energy demand and emissions simultaneously.

“I don’t see major disruption in the actual machine technology,” Pereira adds. “The most disruptive potential is in how mills are using digital integration across the manufacturing process.”

Advanced process control, data analytics and digital optimisation are increasingly viewed as the next frontier of competitiveness. These tools allow mills to improve uptime, reduce variability and optimise energy and water consumption, often delivering faster returns than large mechanical upgrades.

Looking ahead, Pereira is unequivocal: “By 2035, fully integrated, data driven manufacturing will be standard.”

Energy, water and a regional sustainability divide

Energy intensity remains a defining issue, particularly in North America where TAD technology dominates. While TAD is inherently energy intensive, Pereira does not see it losing relevance: “I don’t see TAD becoming less popular,” he says. “Demand for TAD products is still high, and growth remains significant.”

However, sustainability priorities differ sharply by region. In Europe, decarbonisation and water efficiency continue to shape investment decisions. North American producers, by contrast, tend to weigh sustainability investments against local energy prices and availability.

Canada presents a distinct case. In provinces where hydroelectricity dominates, mills already operate on low-carbon grids. “If most of the energy produced by the utilities is coming from hydro, it’s already green energy,” Pereira says. This reduces the urgency for additional decarbonisation investments, though water usage and operational efficiency remain focal points.

European mills can operate at water consumption levels as low as five cubic meters per ton, compared with closer to nine cubic meters per ton in North America. As Kilpi notes, “That’s a big difference and it shows how strongly regulation and cost pressures influence technology choices.”

At the same time, Chinese producers are increasingly attentive to sustainability optics. Biomass boilers and energy-efficiency upgrades reflect both regulatory and reputational considerations.

Fibre flexibility and strategic resilience

Fibre strategy has become another critical lever in future proofing tissue mills. Most new projects are designed with flexibility in mind, allowing producers to adjust fibre mixes in response to market demand, regulation or cost volatility.

“Almost all the mills we study want to have fibre flexibility,” says Pereira. “They want to be able to use recycled fibre if it becomes cost competitive, or alternative fibres if sustainability requirements increase.” Flexibility is insurance against regulatory change, fibre price volatility and shifting consumer expectations.

Non-wood fibres such as bamboo, straw and bagasse are attracting growing interest, particularly as tools to reduce carbon footprint. Bamboo, Pereira notes, offers fibre properties comparable to softwood, although it is not necessarily cheaper.

Despite experimentation, eucalyptus pulp remains central to tissue quality, especially for softness: “Eucalyptus is used widely because of the softness it delivers,” Pereira says, sometimes accounting for 60–70% of the furnish.

Scale, integration and competitive advantage

Across North America, scale continues to matter. Integrated operations that combine tissue machines and converting lines are increasingly dominant, particularly in Canada, where independent converters have largely disappeared. “When profit margins are measured in pennies per case, scale, and high-speed efficient machines make a real difference,” Pereira says.

Producers with modern assets are consistently outperforming those relying on older machines, even when the latter have larger installed capacity. This dynamic is driving targeted, high-impact investments.

Outlook: toward a more digital, flexible future

Asked for bold predictions, Martin Pereira strikes a hopeful but pragmatic tone. His central expectation is that sustainability and decarbonisation will regain momentum and be supported, rather than replaced, by digitalisation.

“My hope is that the focus on sustainability and decarbonisation comes back and becomes the norm,” he says. “Combined with integrated, digital operations, that’s what will define future-ready tissue manufacturing.”

For Kilpi, adaptability is equally critical, balancing performance, aesthetics and efficiency across regions. While regional differences will persist, the direction is clear: smarter mills, faster decisions and a relentless focus on efficiency. As the North American tissue sector moves forward, the winners will be those who can navigate rising costs, leverage digital tools, and align investment decisions with both market realities and long-term resilience.