As it accelerates sharply, the way value is created, defended and contested is changing rapidly. Liying Qian, Euromonitor International, Global Insight Manager – Tissue and Hygiene asks what underpins tissue’s demand resilience and where are the emerging risks?

Despite persistent cost inflation and economic uncertainty, consumer tissue demand proved resilient in 2025. Global volume growth remained modest and broadly in line with 2024, but nominal value growth accelerated sharply, reinforcing a structural shift toward price‑ and mix‑led expansion rather than incremental usage. This value‑driven growth pattern is expected to intensify in 2026, signalling a market increasingly shaped by affordability gaps, premiumization and uneven consumer trade‑offs.

This shift raises a critical question for the industry: what underpins tissue’s demand resilience and where are the emerging risks? Structural fundamentals such as population growth and income expansion continue to anchor long‑term demand, but the way value is created, defended and contested is changing rapidly.

The staying power of Asia

Many of these forces are most visible in emerging markets, where demand resilience is both reinforced and tested. In 2025, emerging economies accounted for 45% of global tissue value sales, up from 42% in 2020, led by China, Brazil and Mexico. While rising incomes and population growth continue to support baseline demand, heightened price sensitivity is creating sharper divergence in how consumers define and access value.

Asia Pacific stands out as the most influential region, representing 43% of global tissue volume but only 31% of value in 2025. Expanding middle class consumption from a low per capita base presents meaningful upside, yet competition is intense. E-commerce accounted for 28% of APAC tissue sales, well above the global average, and players outside the top five represented nearly 70% of regional retail tissue value. This fragmentation underscores how local brands and digital routes to market are eroding traditional multinational scale advantages.

As a result, growth in emerging markets is increasingly driven by localization, simplified propositions and sharp price per use positioning, with e-commerce accelerating trial, brand discovery and speed to scale.

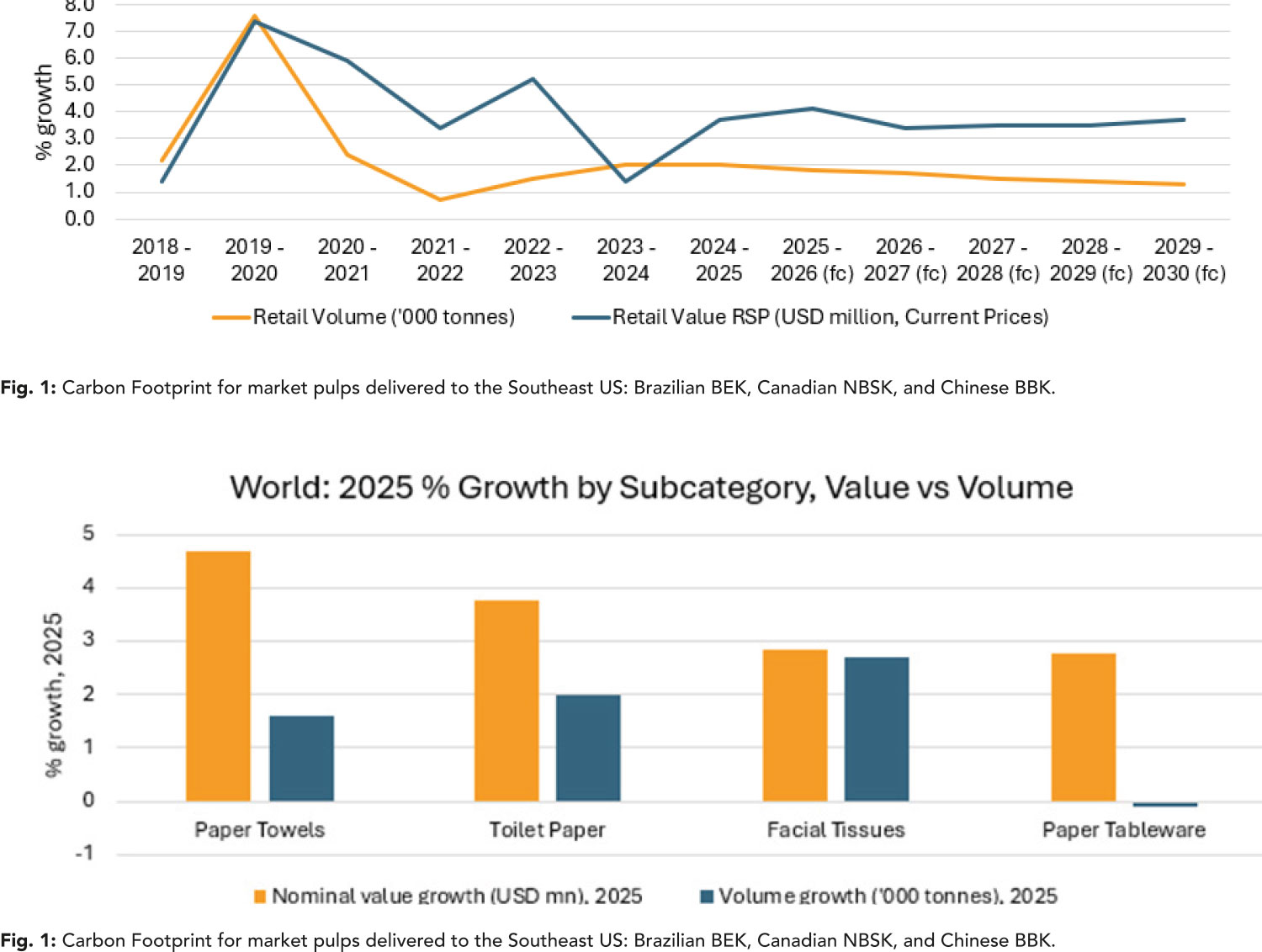

Wellness-tied and tasks-driven tissue types lead growth

Beneath overall demand stability, tissue category performance is becoming more uneven. Growth is less about increasing usage frequency and more about how consumers trade between formats, pack sizes and quality tiers, reinforcing a shift from volume expansion toward mix‑driven value creation.

Toilet paper continues to anchor volume in absolute term through habitual usage and expanding population and penetration in emerging markets, but growth is structurally constrained in developed economies. By contrast, paper towels and selected facial tissue formats are outperforming, benefitting from perceived multifunctionality, hygiene reassurance and convenience across both at‑home and on‑the‑go occasions.

In Asia, facial tissues receive an additional lift from wellness‑ and skin‑care‑led positioning, reflecting stringent beauty standards and rising incidence of allergies, colds and seasonal illness. Meanwhile, more discretionary or occasion‑dependent segments, such as napkins in some markets, face substitution pressure and softer demand.

Tissue competition sharpens as scale, value and integration redefine the leaderboard

As growth becomes increasingly mix driven rather than volume led, competitive intensity is rising, with share gains coming primarily from redistribution rather than category expansion. Private label and value oriented local brands continue to strengthen their foothold in commoditized tissue segments by pairing aggressive price per use propositions with improving perceived quality and faster adaptation to local usage needs.

Innovation has become more selective and execution focused. Instead of breakthrough functionality, activity centres on format optimisation, pack and sheet engineering, durability cues and incremental premium signals such as softness, ply structure or absorbency. Sustainability claims are more visible, but in most markets remain supportive rather than decisive, particularly when they introduce clear price premiums.

The result is a more polarised competitive landscape. Scale, efficiency and cost discipline increasingly define success at the core, while targeted premiumisation and branding are used selectively to defend value. Softys stands out among global leaders by consistently gaining tissue share through scale driven execution rather than innovation, leveraging acquisitions, notably in Brazil, to expand capacity and geographic reach, and aligning strong local manufacturing with value focused brands. Recent consolidation reinforces this structural shift: RGE’s acquisition of Vinda secures full pulp-to-issue integration in Asia, while Kimberly-Clark’s international tissue exit via the Suzano joint venture signals a pivot toward regional integration and volatility management.

What comes next?

These dynamics point to a decisive moment for the tissue industry, as value creation shifts toward precision: what it takes to win in an increasingly fragmented, value led market?

At Tissue World Miami 22-24 April, Euromonitor International will explore the key forces shaping consumer tissue demand and competitive strategy: from evidence-backed value propositions and experiential wellbeing to hypersegmentation and sustainability.