As the retail experience continues to expand across increasing outlets, companies look to key sectors including hygiene, sustainability, e-commerce and aesthetics, as dramatic M&A activity continues. And “to re-introduce excitement to a very established space.” Report by Ashley Mandel, Research Associate, Euromonitor International.

Retail tissue in the US in 2025 underwent overall consistent value growth compared to 2024. Unit price growth remained soft as inflation lowered and companies pulled back on steep price increases in 2025 as they are absorbing cost increases associated with materials, supply chain, and tariffs.

Overall, the category witnessed softer volume gains, higher quality and more absorbent private label offerings. Equally, consumers remained price-sensitive and pulled-back on household spending across the board. In regards to modest unit price growth in 2025, private label brands continued to take up more of a share of purchases in the tissue and hygiene space. Additionally, consumers made more purchases through club stores offering bulk discounts on tissue products.

Demand for premium tissue products in the US continues to rise, driven by consumer preference for softer, stronger, and higher-quality options. In 2025, companies invested in TAD paper machines, which, despite longer production times, deliver superior softness. Today’s consumers expect ultra-soft, strong, and highly absorbent tissue products from both private labels and national brands.

Another significant trend in tissue market is sustainability, with consumers demanding ecofriendly products, biodegradable packaging and pushing innovation towards recycled/alternative fibres such as recycled pulp, bamboo. It has been seen that tissue products with added natural elements like aloe vera or almond oil for soothing properties are more popular among consumers. Sustainability as a trend is particularly more important in paper towels, in which the focus on reusability and recycled content is growing, given that paper towels are often used for quick, everyday tasks, which can sometimes result in excessive waste.

Executive summary: American tissue in 2024 and 2025

Tissue and hygiene in the US has witnessed continued current value growth in 2024 and 2025, although this was slower than in previous years due to the easing of the strain on price growth and inflation. While unit price growth was comparatively lower in 2024 than in the previous year, there remained a complicated relationship regarding labour shortages, costs of pulp, and spending.

In terms of retail tissue, a softer current value increase and stronger volume performance was seen due to slower unit price increases, which encouraged some consumers to re-engage with household brands and sustainable premium options; albeit this was also alongside the growth of private label offerings. Although private label had already been winning in retail tissue for a couple of years due to price rises and cost concerns when it came to branded products, it continued to see retail value sales and share growth, through price guarantees and quality improvements. Such actions have solidified private label products as a go-to choice amongst US consumers, continuing to outperform many brands, and driving growth within retail tissue, especially in toilet paper, paper towels, and boxed facial tissues.

On the AfH tissue side, volume and current value growth were seen as return-to-office policies continued to normalise tissue consumption levels post-pandemic. This was also driven by a return to travel.

In 2024-2025, retail toilet paper remained the largest category within tissue and hygiene and continued to grow in both volume and current value terms, winning consumer dollars through quality improvements and private label cost-benefit delivery. Private label once again outperformed legacy brands due to the consumer proclivity for buying on promotion or buying in bundles. For the past couple of years private label has innovated in improving private label pulp quality, attracting consumers’ attention due to comparable quality to branded products. Aside from private label wins, premium Direct-to-Consumer (DTC) brands also underwent exciting transformation, as the sustainable toilet paper brand Who Gives A Crap? entered into offline retail at US Whole Foods locations, confirming consumers’ interest in premium, sustainable toilet paper products at premium retailers.

To meet changing consumer demands a host of new product launches have been recorded which emphasised skin-nourishing ingredients such as vitamin E and almond oil, and featured citrus aromas, and plant-based organic fibres such as bamboo. Elevated product compositions and functionalities continued to cater to consumers who prioritise skin concerns, such as preventing infections and maintaining skin pH. The pervasiveness of sustainable fibre-tissue products such as bamboo, organic cotton, and recycled pulp continued to lead innovative product launches across toilet tissue and hygiene.

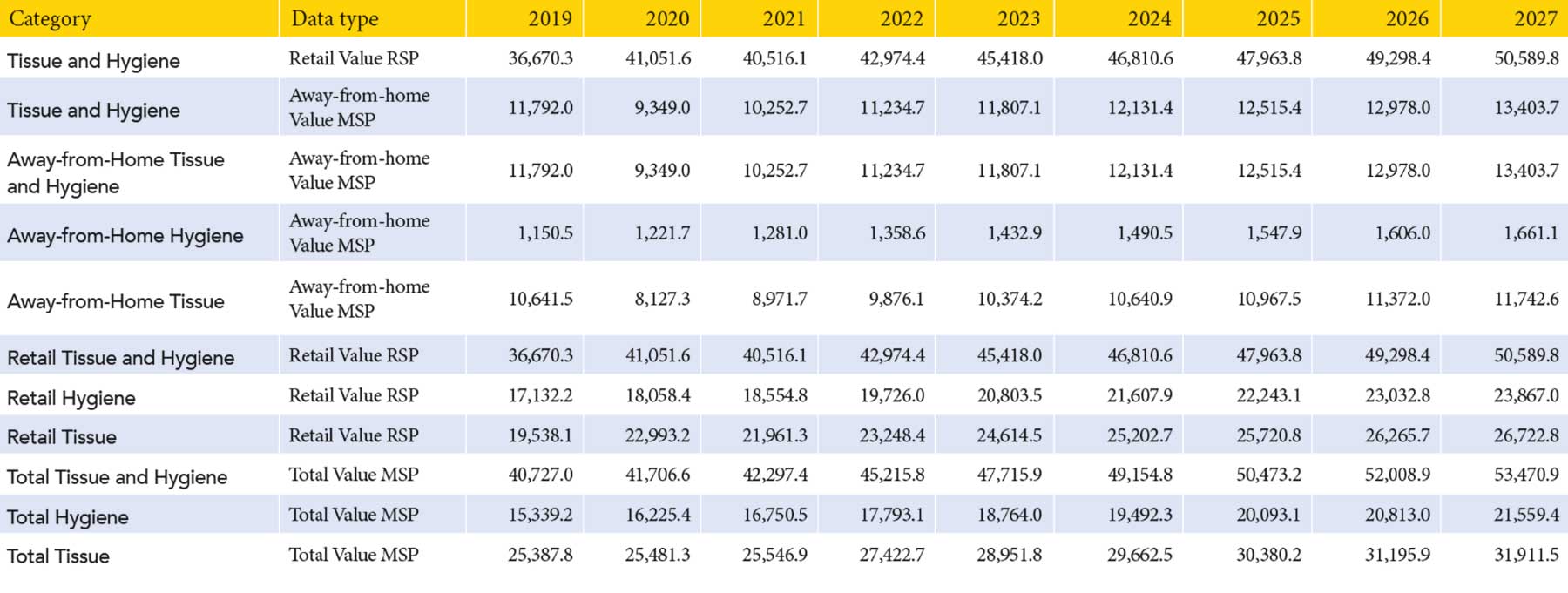

All content relates to the USA, units are in USD millions and all constants are current prices.

Another significant trend influencing tissue and hygiene has been the heightened focus on sustainability, which involves utilising plant-based materials and minimising the environmental impact post-consumption. Companies have been enhancing their sustainable credentials by partnering with environmental organisations to reduce landfill waste and support purpose-driven initiatives. This commitment to community engagement and carbon footprint reduction positively influences brands’ reputation and public perception. However, whether these initiatives directly affect a company’s profitability remains a key strategic consideration.

Retail developments

Hypermarkets remained the largest distribution channel for retail tissue and hygiene in the US, as many people purchase these products along with their weekly grocery shop for convenience reasons. Hypermarkets also offer a wide product range in terms of brands and pack sizes, and prices are reasonable, especially when buying in bulk. However, retail e-commerce saw the strongest value share growth, with this channel especially popular for hygiene products.

Categories have benefited from the continued expansion of retail e-commerce, where consumers can research and compare products with ease. Similarly, DTC brand entrants, particularly those offering premium, female-focused and natural-positioned products, have quickly garnered traction on social media. Purchasing large packs of relatively lightweight fibre-based products without the hassle of cumbersome transportation is a prime benefit of online retail channels. The appeal of buying in bundles at warehouse clubs or buying online with the ease of at-home delivery or auto-delivery subscription from online market spaces also rings true in retail tissue categories, most notably impacting toilet paper and paper towels.

Amidst economic uncertainty, consumers have been seeking ways to maximise their spending. Discounters and warehouse clubs offer household goods at budget prices, and therefore maintained solid sales growth in 2024, with discounters performing particularly well. Their private label and bulk offerings, paired with a stripped-down in-store environment, enable such discount retailers to undercut supermarkets. Warehouse clubs allow shoppers to purchase essentials in one trip, providing convenience and fuelling the pre-emptive price hike and bulk-buying mentality. Transformations in retail distribution over the forecast period are expected to be shaped by cost, convenience, and customer loyalty.

What next for tissue and hygiene

Tissue and hygiene in the US is set to see stable current value growth rates in the forecast period, with increases for both retail tissue and hygiene and AfH tissue and hygiene. Within retail tissue, although growth is expected to continue, paper towels could witness headwinds from the reusables sector, as reusable paper towels are slowly gaining favour due to waste reduction and sustainability efforts in the US. Meanwhile, facial tissues are expected to see growth, as the intensifying effects of global warming blur seasonality and elongate allergy seasons, which will extend the use of facial tissues.

In terms of distribution, as retail e-ecommerce further integrates itself as a key channel for all retail tissue and hygiene categories over the forecast period in the US, it will be crucial for brands to adopt a multichannel strategy and include all of their brand offerings in both online and offline retail spaces. While online marketplaces may be top-of-mind for many consumers, other retailers will need to strengthen ways of funnelling sales to their e-commerce platforms and establish mutually beneficial partnerships with marketplace collaborators. At the same time, bricks-and-mortar stores will have to focus on enhancing in-store experiences and expanding their sustainable product offerings to meet the growing consumer demand for eco-friendly options and aesthetically packaged paper products to re-introduce excitement to a very established space.

Products incorporating plant-based fibres are expected to continue to gain shelf space as consumers become more informed about their natural skin benefits. Challenges such as raw materials sourcing and the higher cost of plant-based alternatives compared with conventional materials may slow growth. Despite this, in the premium retail hygiene segment plant-based fibres represent the future of product development. Mass-market brands, while less likely to fully transition to plant-based materials, may still position themselves as more skin-friendly by highlighting the removal of parabens and potential irritants such as fragrances on their packaging.

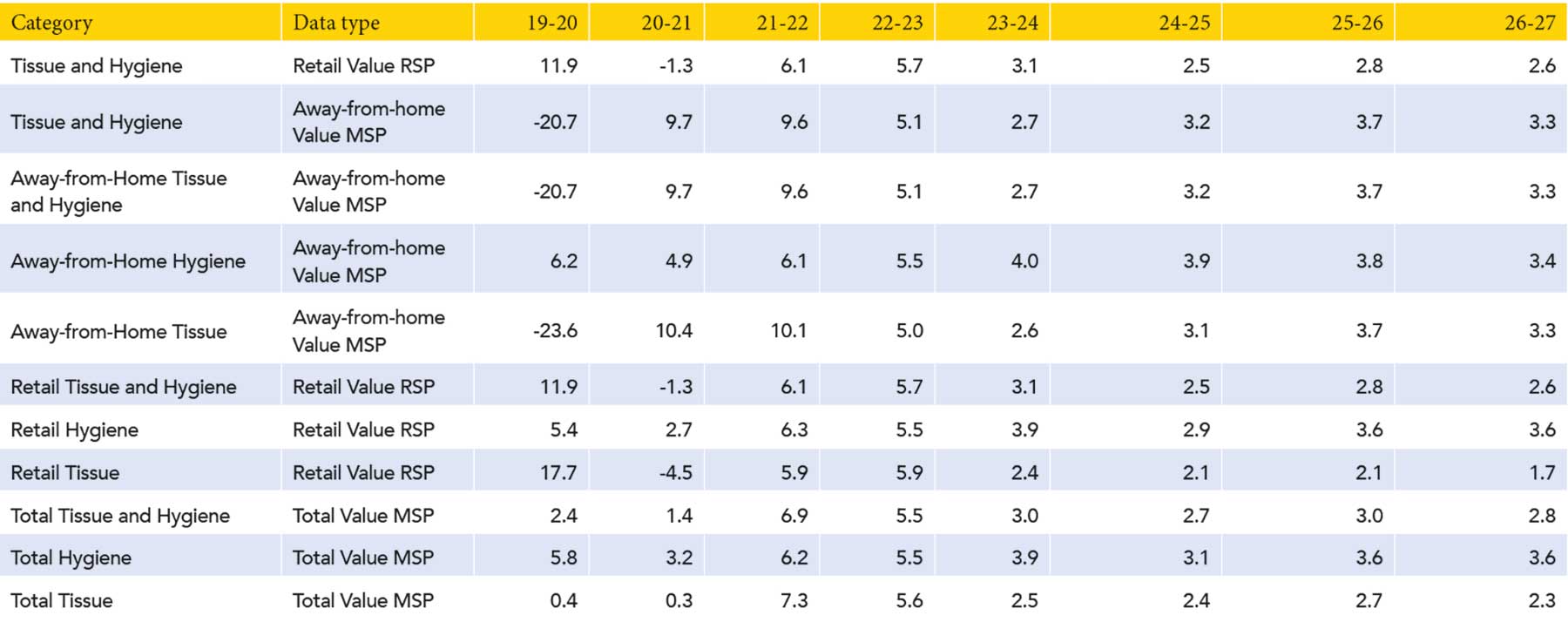

All content relates to the USA, units are in USD millions and all constants are current prices.

AfH Tissue and hygiene in America: May 2025

Key findings

Value sales msp rise by 3% in current terms in 2024 to $12.1bn

AfH hygiene is the best performing category in 2024, with value sales msp rising by 4% in current terms to $1.5bn

Sales msp are set to grow at a current value CAGR of 3% (2024 constant value CAGR of 1%) over the forecast period to $14.0bn.

Growth in AfH tissue driven by quality expectations and policy changes

AfH tissue in the US posted positive current value and volume growth, although the rates of increase were slower than in the previous few years. Sales continued to climb towards their pre-pandemic baseline, with return-to-work policies implemented by companies and the return to socialising and travel contributing to growth.

AfH paper tableware remained the largest category within AfH tissue. However, it should be noted that despite seeing slight current value growth, it saw volume decline, and sales remained lower than the pre-pandemic (2019) level. This was due to the decline for AfH tablecloths, because more businesses ceased to use paper tablecloths, either removing these completely, or turning to cloth variants. Nevertheless, the decline for AfH tablecloths was offset to some extent by the growth for AfH napkins, which was seen due to the rise in quick and easy drive-through offerings, which are handed over with napkins already in the bag.

Meanwhile, AfH boxed facial tissues saw the strongest volume and current value growth in AfH tissue in 2024, due to global warming extending and exacerbating the symptoms of seasonal ailments such as allergies, colds and flu, leading to increased usage of such products. A rise in demand for sustainable and eco-friendly AfH tissue products was seen, as more businesses and consumers prioritised environmental responsibility. Innovations in product quality and packaging mainly circulated around companies focusing on enhancing durability, softness, and hygiene, while reducing waste.

Prospects and opportunities

Growth and recovery in AfH tissue in the US is expected to continue to be determined by return-to-work policies implemented by companies, while return-to-work and global warming will drive growth for AfH boxed facial tissues. AfH tissue and hygiene is expected to maintain slow and stable retail current value growth throughout the forecast period, with increases anticipated for both AfH tissue and AfH hygiene.

Increased hybrid or returning-to-work practices are likely to contribute to healthy performances for AfH toilet paper and AfH paper towels in the US. Nevertheless, although rising from a low base, AfH boxed facial tissues is expected to see the strongest increases within AfH tissue due to global warming and the resultant higher number of allergies, colds and flu.

AfH tissue and hygiene expected to witness increased mergers and acquisitions activity

Manufacturers within AfH tissue and hygiene in North America have experienced a dramatic number of changes within the past five years in terms of mergers and acquisitions, and many established players choosing to forego the AfH channel to focus on the retail or private label side of production. AfH tissue in the US market is poised to see more mergers and acquisitions in the coming years, due to several driving factors. First, increasing consumer demand for sustainable products is pushing companies to strengthen their eco-friendly offerings, prompting larger players to acquire smaller firms with innovative, sustainable technologies, or niche product lines. Second, the rising costs of wood pulp and labour, and the need for efficient production systems are encouraging consolidation, as merging allows companies to streamline operations, reduce costs, and achieve economies of scale. Due to the above factors, AfH is expected to see consolidation of business operations at a higher rate than retail due to increasing incentives for companies to realign their strategic priorities and focus on more profitable segments.