Urban expansion, demographic shifts and channel evolution reshape hygiene demand across the GCC. By Isam Arshad, Consultant, Euromonitor International.

As 2026 progresses, the Middle East tissue and hygiene sector continues its resilient trajectory, transitioning from broad-based expansion to more disciplined, strategically driven growth. Anchored by the Gulf Cooperation Council markets of Saudi Arabia, the United Arab Emirates, Qatar, Kuwait and Oman, and supported by developing markets such as Iraq and Jordan, the region continues to benefit from metropolitan development, economic diversification and rising hygiene awareness.

In 2025, the Middle East retail tissue and hygiene market has moved beyond its earlier transformation phase. The structural shifts that reshaped pricing, channel dynamics and consumer expectations are now embedded. The region has entered a more mature growth cycle defined by demographic realignment, digital channel penetration and increasingly structured retail execution. Retail value sales are expected to grow at around 3% year-on-year, pushing the market above $3bn.

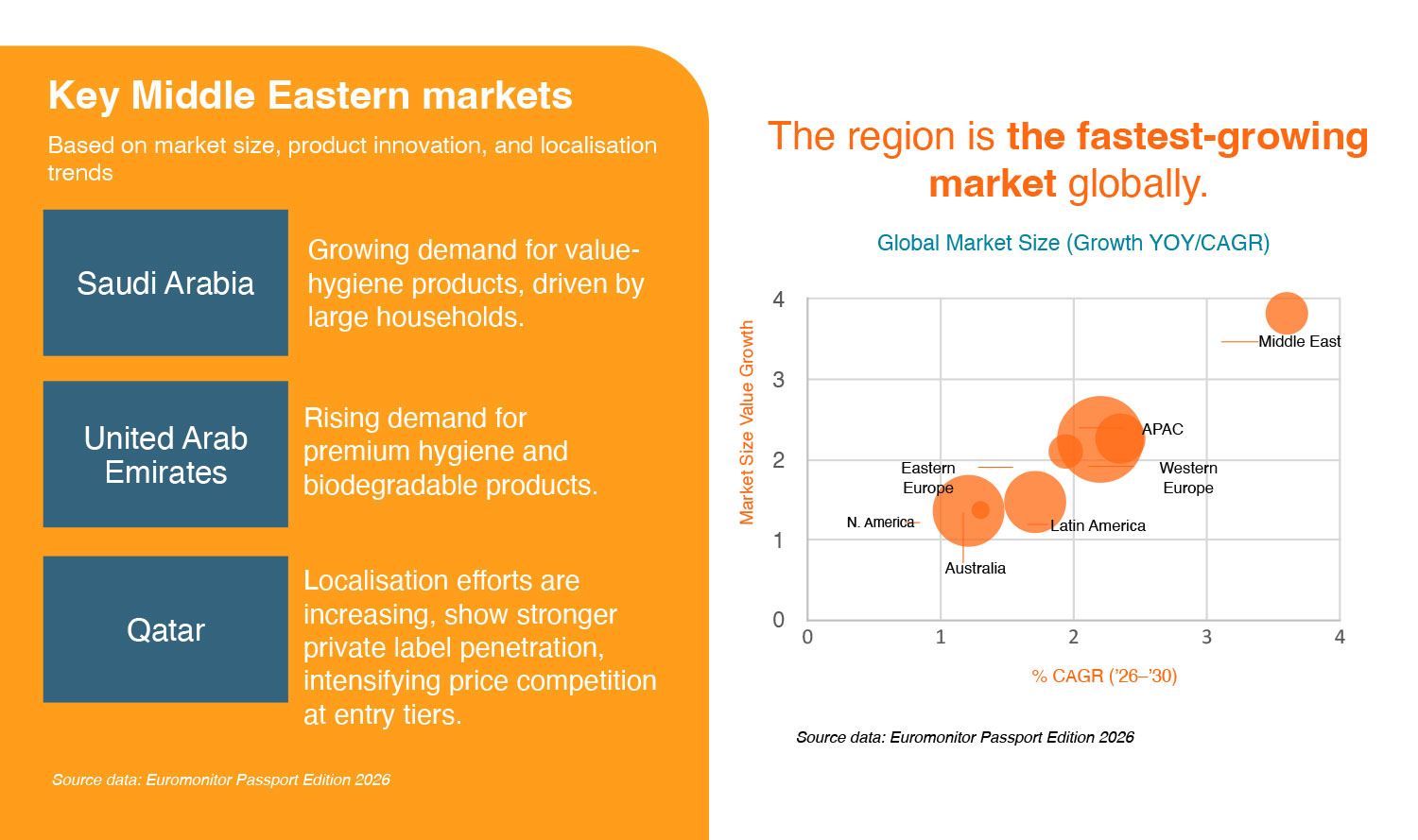

Across Saudi Arabia, the United Arab Emirates, Qatar, Kuwait and Oman, retail tissue and hygiene continue to expand at steady rates. Saudi Arabia remains the region’s largest retail market, exceeding SAR5bn in value sales. The UAE follows as the most dynamic, surpassing AED2bn and recording the strongest recent growth among major GCC markets. Qatar, Kuwait and Oman continue to post stable expansion, supported by rising household formation, urban household consolidation and sustained hygiene awareness.

Urban households and digital retail redefine purchasing patterns

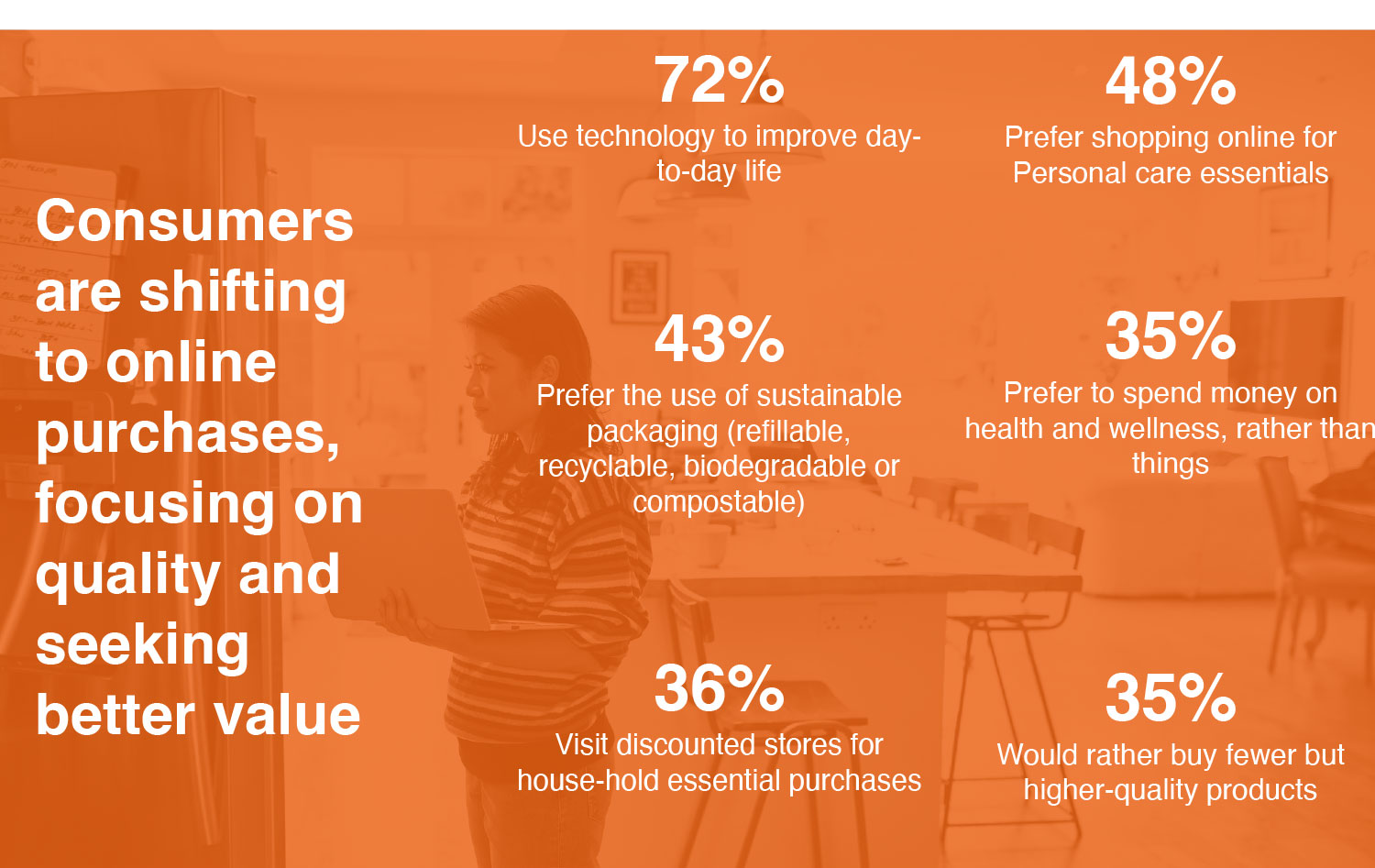

Expanding metropolitan lifestyles across Saudi Arabia and the UAE continue to reshape retail consumption habits. Busier routines, rising female workforce participation and higher per capita incomes are reinforcing demand for convenience-driven categories such as paper towels, wipes and premium facial tissues.

Retail channels are evolving in parallel with these behavioural shifts. In the UAE, e-commerce now represents a meaningful share of tissue and hygiene value sales, while Saudi Arabia continues to record steady gains in digital penetration. Kuwait and Oman are accelerating from smaller bases, supported by improved logistics infrastructure and wider digital payment adoption.

This channel evolution is reshaping pricing architecture and pack strategy. Larger formats, multipacks and subscription-based purchasing models are gaining traction online. Retail competition is no longer confined to physical shelf space; digital presence now directly influences brand visibility, pricing transparency and promotional effectiveness.

At the same time, private label development varies across markets. The UAE and Qatar exhibit stronger private label penetration, intensifying price competition at entry tiers. Saudi Arabia remains predominantly brand led, enabling established manufacturers to maintain stronger positioning within premium segments.

Retail growth in 2025 is therefore being shaped as much by channel dynamics as by underlying consumer demand.

Inflation-led value sensitivity and health expectations prompt portfolio segmentation and value-creation innovations

With inflation easing in 2026, consumers are balancing tighter budgets with continued health and hygiene priorities, prompting manufacturers to segment their portfolios more clearly across price tiers. In Saudi Arabia and the UAE, where affluent consumers continue to trade up, brands are reinforcing premium positioning through eco-friendly materials and hypoallergenic features that justify higher price points. For example, Fine Hygienic Holding’s (FFH) FINE Green line, produced from 100% recycled paper, responds directly to growing sustainability awareness while addressing value considerations. Similarly, Napco’s Sanita Platinum range emphasises enhanced softness and comfort, supporting category premiumisation and portfolio diversification.

In Oman and Kuwait, private label penetration stands at 2.0% and 10.2% respectively in 2025, encouraging retailers such as Majid Al Futtaim’s Carrefour to expand scented and skin-comfort variants while strengthening in-store visibility through strategic shelf placement. Qatar, with private label accounting for 13.0% of value sales, faces sharper entry-tier competition, prompting branded players to refine good-better-best positioning strategies. This structured segmentation supports value growth across the GCC, even as moderating birth rates in markets such as Qatar place constraints on nappies volume expansion.

Demographics shift the category balance

The most important structural shift across the GCC retail hygiene landscape is demographic and behavioural evolution.

Historically rooted in water-based traditions shaped by religion and cultural practice, hygiene habits across the region continue to evolve alongside metropolitan development. Consumers are increasingly blending global hygiene standards with local preferences, reinforcing demand for tissue products without abandoning cultural norms.

In 2026, digital retail is accelerating this transition. E-commerce penetration reached 6% in Saudi Arabia and 13% in the UAE in 2025, with continued upward momentum. Platforms such as Noon are expanding category reach through consumer reviews, bulk promotions and subscription models, particularly in wipes and paper towels. Retailers such as Lulu Hypermarket are leveraging digital analytics to refine product positioning and tailor promotions based on purchasing data.

Sustainability is increasingly important to consumers and is gaining measurable traction. In the UAE, 42% of consumers expect climate change to have a greater impact on their lives, while more than 25% actively seek to reduce environmental impact through everyday purchasing decisions. This growing awareness supports demand for recycled and responsibly sourced tissue innovations.

Although the Middle East accounts for roughly 2.5% of global tissue consumption, its combination of demographic growth, digital acceleration and rising sustainability awareness positions the region for steady long-term retail demand.

Adult incontinence becomes the structural growth pillar amid ageing populations

Adult incontinence is now the fastest growing hygiene category across several Gulf markets. Ageing populations in Kuwait, Qatar, Oman and Saudi Arabia are increasing category penetration, supported by improved product awareness and pharmacy distribution expansion.

Local drive for economic diversity and supply chain resilience drives production localisation

A push for localisation fortifies resilience in 2026, mitigating import risks in a volatile global landscape. The Middle East’s diversification agenda fuels domestic manufacturing investments, generating jobs and enabling custom fits to regional needs. FHH exemplifies this with energy-efficient supply chains, boosting adaptability and cost savings. Such moves not only spur growth but align with sustainability, as in Hayat Kimya’s third-party verified “Papia” brand from responsible sources.

In the UAE and Saudi Arabia, online purchasing is further accelerating adoption by offering discretion and convenience.

In contrast, nappies growth is moderating in markets where birth rates have stabilised. This shift is gradually rebalancing retail hygiene portfolios. Manufacturers that historically relied on baby care as their primary growth engine are increasingly investing in adult incontinence innovation and format diversification.

The region’s demographic profile is reshaping category leadership.

AfH recovery complements retail strength

While retail remains the dominant value driver, away from home tissue demand is recovering across Saudi Arabia, the UAE and Qatar. Tourism expansion, large scale infrastructure projects and hospitality development are supporting demand for paper towels and boxed facial tissues in commercial spaces.

In summary, the defining growth narrative in 2025 remains retail. Household purchasing behaviour, digital penetration and demographic change are driving most value development.

The Middle East tissue sector has matured. It is no longer characterised by rapid market expansion alone. It is now defined by structured retail growth, channel evolution and demographic alignment. Overall, the future of the tissue and hygiene sector in the Middle East will most likely be determined by a combination of customer preferences, digital and supply chain improvements, sustainability drive, and broader economic and cultural trends. The manufacturers that can adjust to these shifts and provide products that are in line with the ever-evolving requirements of their target audience are likely to find success in this fluid market.