As capacity growth slowed in traditional production hubs, new entrants are maintaining across the board, high-quality development. Report by China National Household Paper Industry Association (CNHPIA).

During 2025, China’s tissue paper industry continued to invest in new production capacity, with ongoing innovations in products and improvements in quality. New technologies and equipment have been applied more widely, export scales have expanded further, and upstream and downstream enterprises in the industry have collaborated to explore potential opportunities and enhance efficiency. In an increasingly fierce market competition, the industry has navigated through challenges and striven for development.

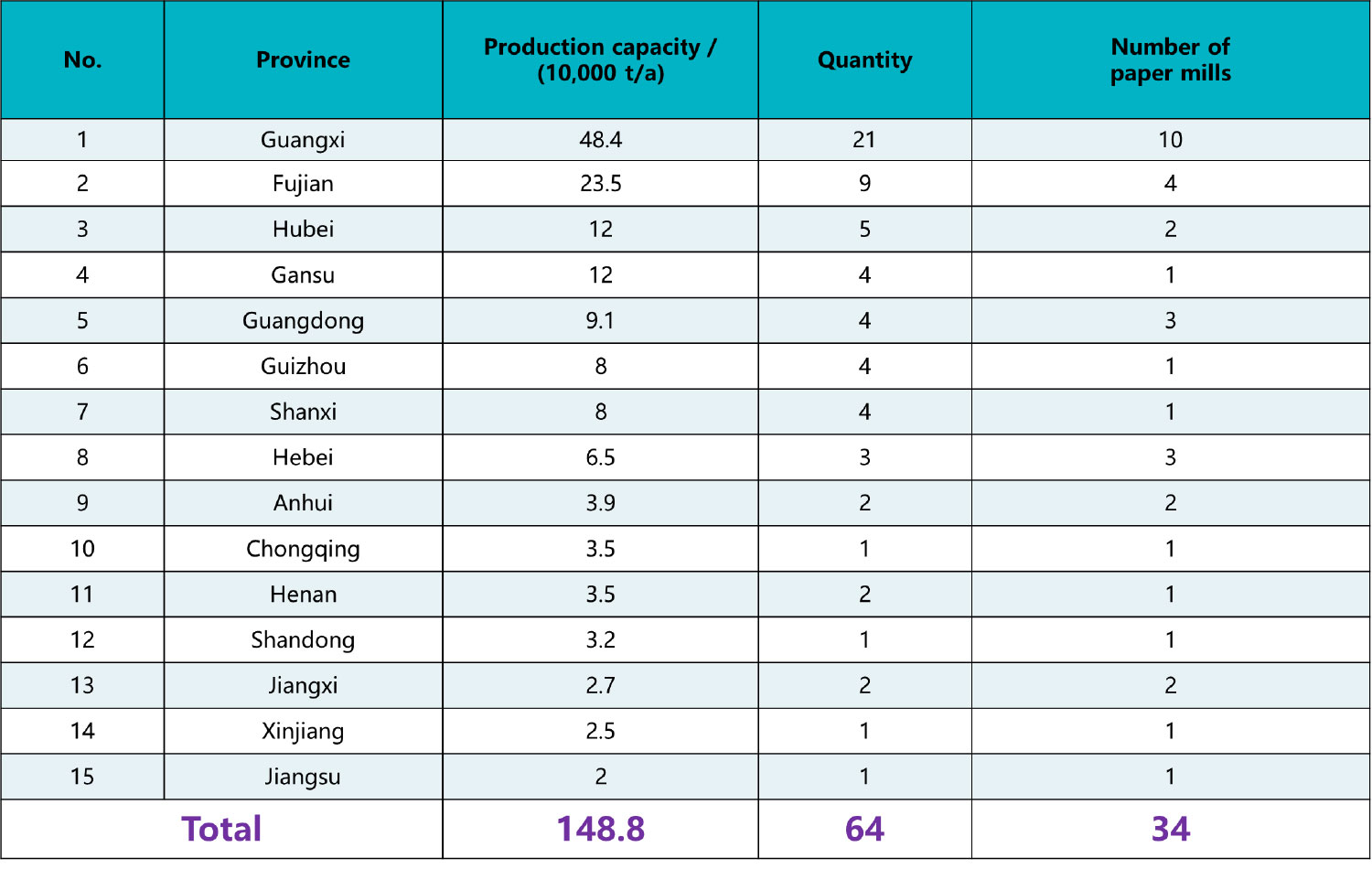

1 / New production capacity in 2025

In 2025, the industry added approximately 1.488m tonnes per year of modern production capacity. The substantial introduction of new capacity has intensified competition within the industry.

The new production capacity spans 15 provinces, municipalities, and autonomous regions, with 34 enterprises collectively commissioned 64 paper machines. Of these, 57 were domestically manufactured, accounting for the majority. The newly added capacity is primarily concentrated in areas such as Guangxi, Fujian, Hubei, and Gansu.

Capacity growth has slowed in traditional production hubs like Hebei Province and emerging hubs like Shanxi. In 2025, Fujian Province saw 235,000 tonnes per year of new production capacity, mainly contributed by leading companies such as Hengan International Group and Fujian Botare Network Technology, as well as integrated pulp and paper enterprises like Lian Sheng Paper. Gansu Province added 120,000tpy of capacity, primarily from Gansu Yusen’s new production capacity at its Pingliang base, Gansu.

Integrated pulp and paper producers like Lee & Man Paper, Taison, Sun Paper, and Liansheng Paper continued to expand their capacity. Their newly added production capacity in 2025 was 490,000 tonnes per year. By the end of the year, the total capacity of these five companies reached 4.55m tpy. These enterprises have leveraged their integrated pulp and paper advantages to produce and sell tissue parent rolls, fostering synergies between brand companies and pulp enterprises in the industry chain and achieving complementary strengths and win-win cooperation. Additionally, Xianhe, a new entrant in the tissue industry, put four new crescent tissue machines into production in Jingzhou, Hubei, with a total capacity of 100,000 tonnes per year.

According to the 2024 Annual Report of China’s Paper-making Industry, China’s domestic wood pulp production in 2024 was 26.26m tonnes, with bamboo pulp production at 2.59m tonnes. From January to November 2025, the new domestic wood pulp production capacity amounted to 2.411m tonnes per year, while the new bamboo pulp production capacity was 150,000tpy. Furthermore, in 2025 alone, publicly announced new construction or technological transformation projects for wood pulp and bamboo pulp have collectively added over 13m tonnes per year of new production capacity.

2 / Revenue performance of listed companies

In the first half of 2025, the household paper and wet wipe business of Hengan, as well as the operating revenue achieved by Zhongshun Jierou in the first three quarters of 2025, recorded growth.

In the first half of 2025, Hengan reported sales revenue of tissue paper and wet wipes up 3.2% year-on-year to RMB7.174bn. Sales revenue of tissue paper and wet wipes accounted for 60.8% of the group’s total revenue. Gross profit margin of tissue paper and wet wipes increased to 21.9%.

For Zhongshun Jierou, it reported operating revenue of RMB6.478bn the first three quarters of 2025, representing a year-on-year increase of 8.78%.

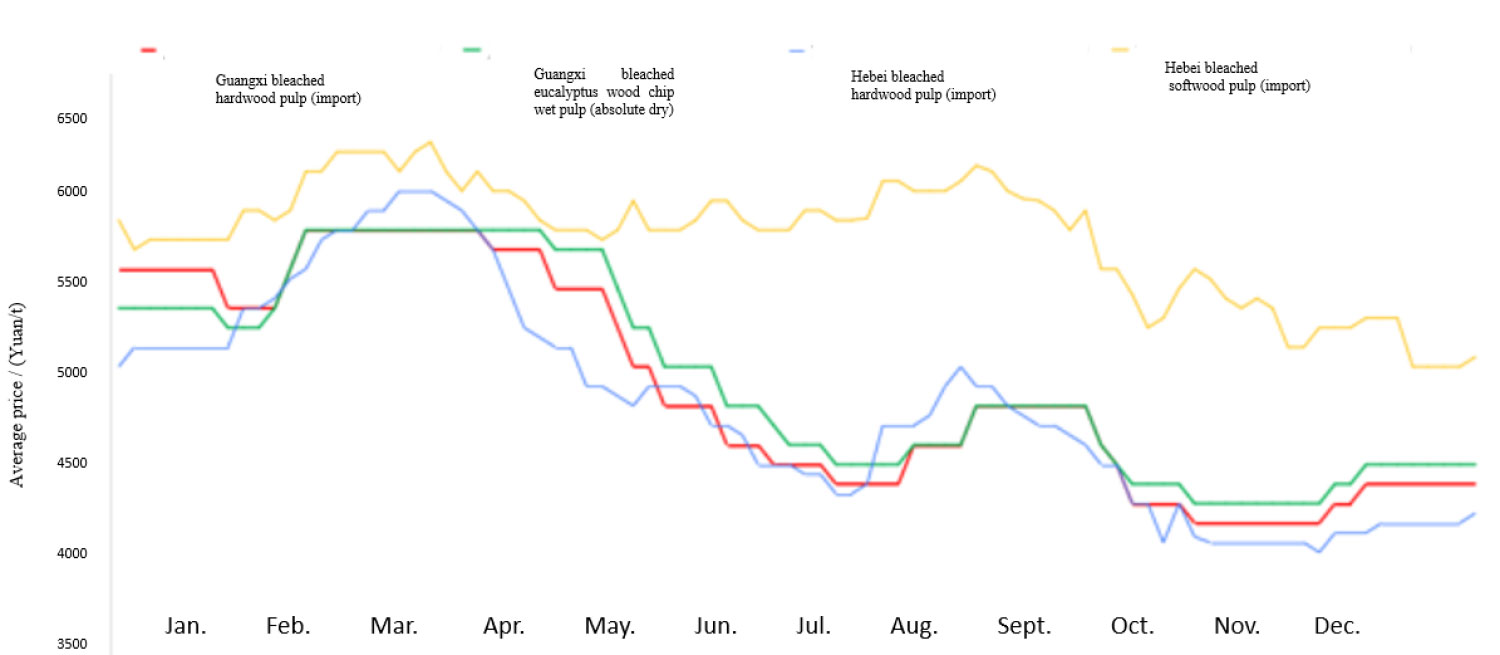

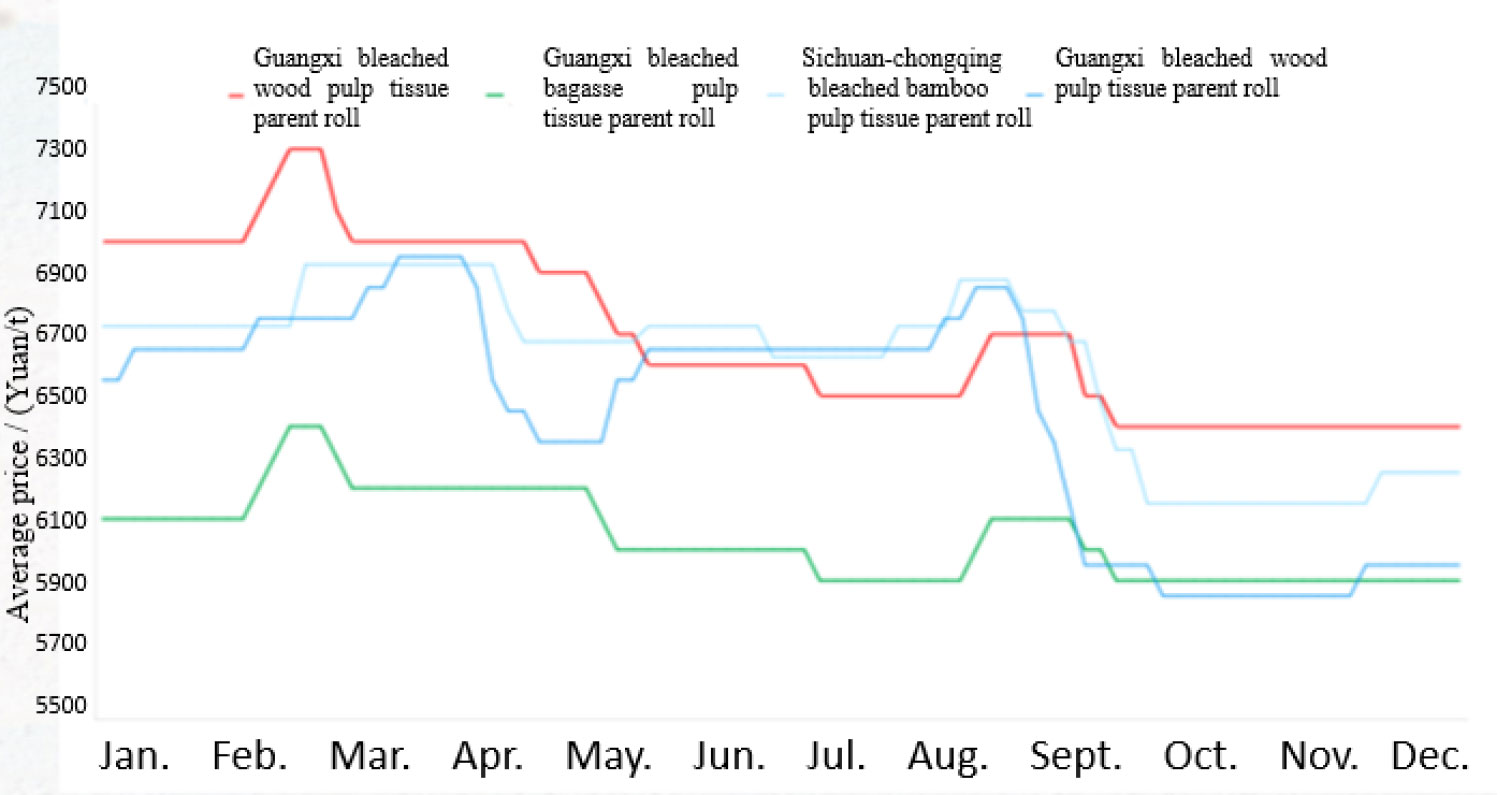

3 / Price changes of pulp and tissue parent rolls

Here are the changes in average prices of pulp and tissue products from January 2024 to December 2025. From the data we have collected, the average spot price of commercial wood pulp in China’s market in 2025 is generally lower than that of 2024, especially the price of hardwood pulp. The average price of tissue parent rolls has declined. These price trends reflect the industry saw ample production capacity and fierce competition.

4 / Product upgrading and innovation

In 2025, tissue companies continued to upgrade their products, achieving differentiation and innovation in embossing, printing, moisturising ingredients, and packaging design, thereby enhancing market competency. Notably, this year saw more companies launching printed facial tissues, handkerchief tissues, and similar products. Furthermore, bottom-dispensing packaging was adopted for more product types, such as kitchen towels and lotion tissues.

5 / The application of new technologies and equipment

Starting with tissue machines: the production capacity of globally advanced TAD and TAD-like tissue machines continues to rise. In 2025, Hengan International Group and Chongqing Longjing Paper both invested in TAD tissue machines; Zhongnan Paper (Henan Base) put into operation another TAD machine made in China.

Domestic hand towel machines now feature wider widths and improved flexibility; Shandong Xinhe Paper-Making Engineering has launched China’s first domestic 5.6m super-wide hand towel machine at LOPIE Paper in Guigang, Guangxi; Baotuo Paper Machinery’s dual-cylinder crescent tissue machines are designed to produce tissue parent rolls for tissues and hand towels, allowing for flexible transitions. This machine has been put into operation at Hongzehu Paper.

Moreover, several new technologies for auxiliary equipment supporting tissue machines have been widely applied, further enhancing the energy efficiency of tissue machines and reducing consumption.

The post-processing equipment has also been optimised and upgraded, incorporating new technologies such as ultra-wide width and internal half-fold techniques, which enhance production efficiency and improve product quality during the post-processing stage.

They included:

- High consistency refiner

- Headbox cascade diffuser

- Soft boot press, double blanket independent boot press and other technologies

- Dual-breathing steam hood, steam condensate water, and hot air recovery system

- Performance upgrade of wire cloth

- White water resource recovery system

- The vacuum pump adopts magnetic levitation, air suspension, and permanent magnet variable frequency technology.

Equipment for processing, packaging, and warehousing

Additionally, further advancements were made in packaging and warehousing equipment, along with intelligent and inspection systems. They included:

(1) Processing equipment (extra-wide, multi-purpose, embossing, internal half-folding technology)

- Ultra-wide (2.9~3.7m) processing equipment

- Embossing and water composite technology

- Folding machine utilising constant vacuum technology

- The first facial tissue with half-folded technology

(2) Packaging and warehousing equipment (multi-functional integration, high-precision control, and green efficiency)

- Complete line solution from single package to palletising

- Laser marking and printing machine

- Satellite printing machine

- Paper bag packaging machine

- The three-dimensional warehouse system is equipped with intelligent software and hardware.

(3) Smart devices (deep integration of AI and automation technology)

- A process macro model that integrates industry knowledge with AIOT technology

- Intelligent inspection robot

- Collaborative palletising robot.

(4) Testing equipment (digitalidation, efficiency)

- By connecting the detection equipment to the data processing workstation through QMS, real-time acquisition and integration of detection data can be achieved.

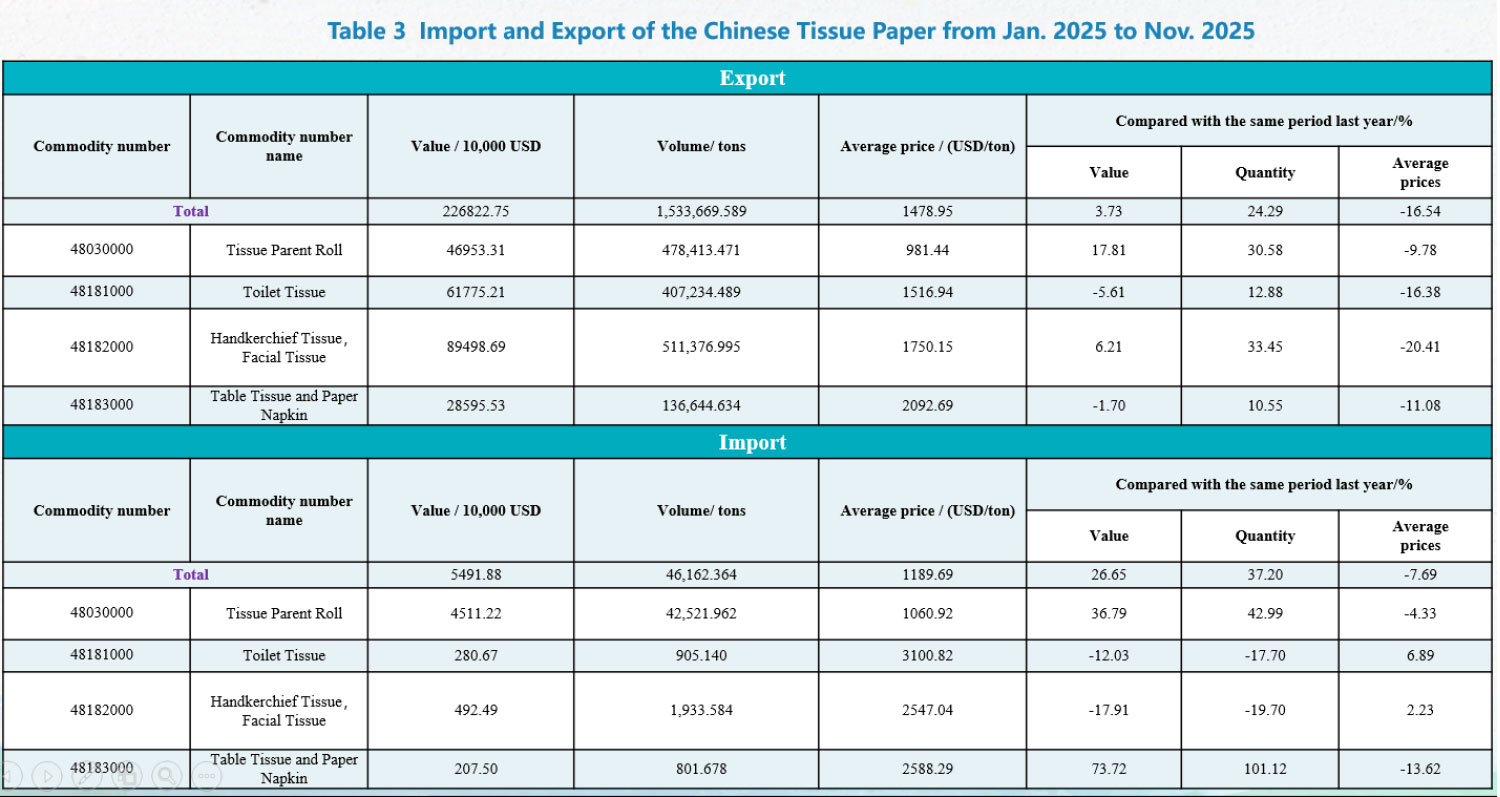

6 / Import and export markets

According to customs data, from January to September 2025, the export volume of tissues increased by 22.46% year-on-year, reaching 1.2148m tonnes. Exports were dominated by finished products, accounting for 68.75% of the total export volume. In terms of the destination countries and regions for China’s tissue exports, the volume exported to the United States decreased, while exports to countries such as Japan, Thailand, Malaysia, the Republic of Korea, the United Kingdom, the Philippines, and Vietnam all saw increases.

The import volume was small, merely 30,570 tonnes.

Despite the growing export volume, some aspects were not that optimistic, a less positive aspect was the year-on-year decrease in export value, indicating a decline in average unit prices. This data illustrates the average export price of exported products from 2014 to the first three quarters of 2025, showing a downward trend since reaching its peak in 2019. This also indicates that competition in the export market is extremely fierce.

In 2025, the export performance of China’s tissue machines achieved a leapfrog advancement. According to the research and summary by the Secretariat of the Hygiene Products Specialty Committee, Baotuo Paper Machinery, Shandong Xinhe Paper-Making Engineering, Changda Machine, Shaanxi Bingzhi Machinery, KILA, Shandong Kaixin Paper Industry, and other equipment manufacturing companies collectively signed contracts to export 66 tissue machines throughout the year, with a total capacity of approximately 1.3m tonnes per year.

In 2025, the export of processing equipment for tissues from China exceeded 500 units/sets. The exported equipment mainly comprises both stand-alone machines and complete production lines, adapting to the needs of customers from different countries. Major export destinations include the Republic of Korea, Türkiye, Egypt, Jordan, and Saudi Arabia.

7 / The release and implementation of industry standards

The standards implemented in 2025 include:

- Hygienic Requirements for Disposable Sanitary Products, General Safety Technical Specification for Infants and Children Paper Products, Green Product Assessment—Paper and Paper Products, and The Norm of Energy Consumption Per Unit Product of Pulp and Paper. The standards under revision include:

- Bathroom Tissue (including Bathroom Tissue Base Paper), etc.

- The national standards under revision include:

- Tissue Paper and Tissue Products – Part 13: Determination of Disintegration, Tissue Paper and Tissue Products – Part 14: Determination of Surface Friction, etc.

8 / Industry energy conservation and emission reduction

In 2025, Photovoltaic (PV) systems saw wider adoption in the household paper industry, with most companies having installed solar power systems for energy conservation. At the same time, enterprises also had their water treatment systems upgraded, with improving water efficiency.

The Shandong Provincial Department of Industry and Information Technology released the list of “Top Performers” in water efficiency among key water-using enterprises for 2025, with three companies – Vinda Paper (Shandong) Co., Asia-Pacific Senbo (Shandong) Pulp and Paper Co., and Shandong Kunsheng Environmental Protection Technology Co. – being shortlisted.

9 / Fulfilling social responsibility

In 2025, companies in the tissue industry continued to fulfil their social responsibilities and engaged in various charitable activities.

Overall, in 2025 China’s modern production capacity and export volume of the tissue industry further increased. Companies in product manufacturing and equipment production continually pursued progress, resulting in improved product quality and advancements in intelligent manufacturing. They have achieved excellent results.

Moreover, enterprises actively carried out their social responsibilities, demonstrating a strong commitment to corporate social responsibility. With the collaborative efforts of both upstream and downstream companies, the tissue industry has taken new strides toward high-quality development.