Retail value sales to continue rising as companies shift their strategies to offset fundamental cultural changes and population decline set to reach 9% by 2039. Report by Euromonitor International’s Senior Consultant Aya Suzuki.

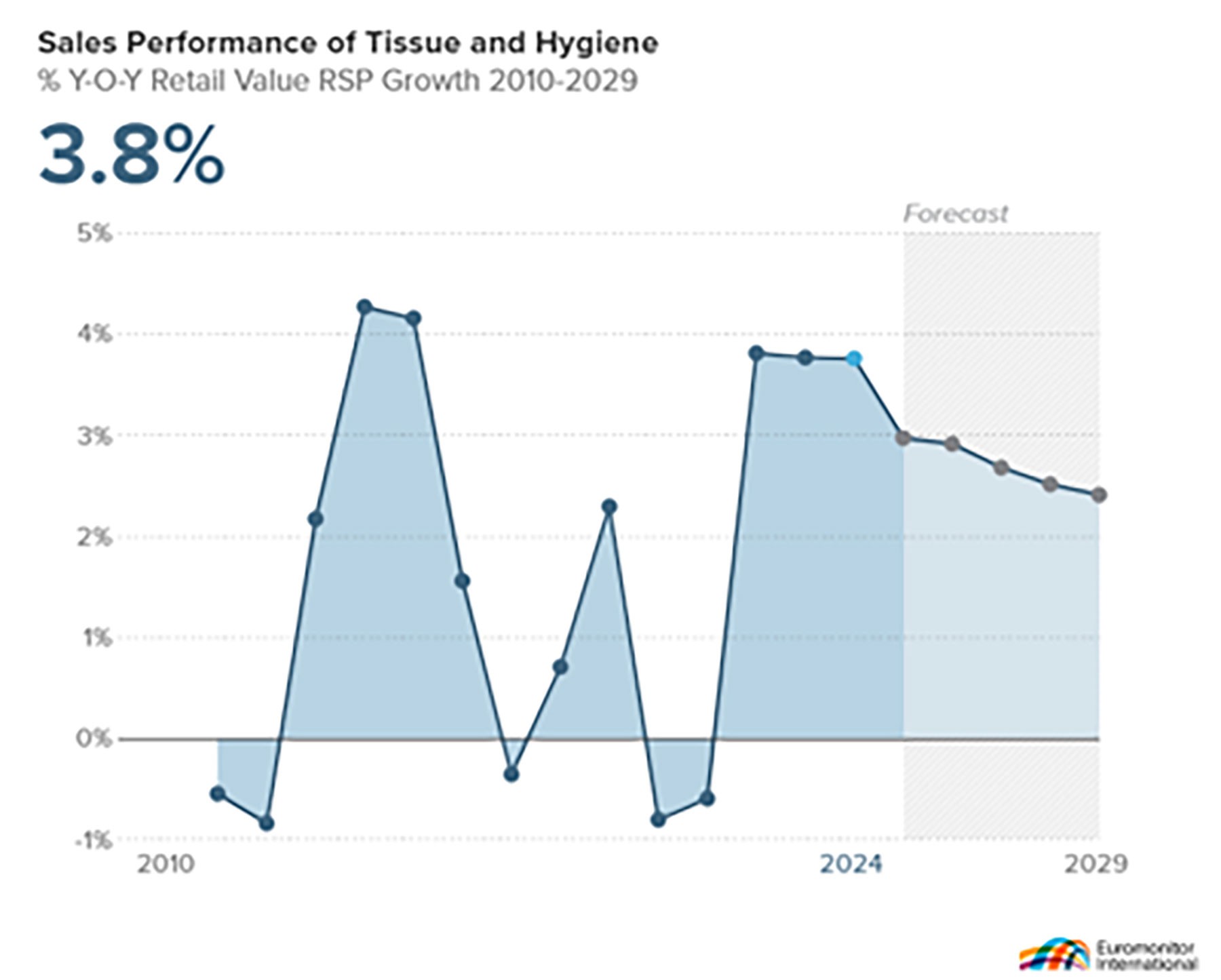

Retail and AfH tissue and hygiene in Japan both maintained solid growth in current value terms in 2024. Value growth was driven largely by inflationary price increases, and an emphasis on high value-added products, which led to rises in unit prices within the market. A notable example of a value-added product with a higher price is Karada Omoino Toilet Roll, launched by Oji Nepia in July 2024. This toilet roll features four layers, boasting an absorption capacity 1.5 times greater than traditional products. In addition, it reduces friction and is designed with a silky-touch finish, which is gentle on sensitive skin. Such innovations demonstrate a shift in strategy amongst companies towards improving profitability and margins through selective focus and concentration on high-quality offerings.

Growth for AfH tissue in 2024 was also driven by growth in the tourism industry in Japan, which has seen a marked recovery following the disruptions caused by the Covid-19 pandemic. According to Euromonitor’s Travel data, the number of inbound arrivals significantly declined in 2020 and 2021 due to various pandemic-related barriers. However, from 2022 onwards recovery began to take shape, with a significant resurgence in 2023, when Japan reclassified Covid-19 as a less risky infectious disease. By 2024, inbound arrivals had already surpassed the pre-pandemic (2019) level, and projections indicate further growth.

2024 key trends

Retail tissue remained the largest category within retail tissue and hygiene in 2024 and saw the strongest current value growth, thanks to high and rising sales of toilet paper and facial tissues. Despite rising prices, consumers did not immediately shift to cheaper product lines or private label. Instead, they continued to choose higher-priced products that emphasised convenience and softness. The convenience and comfort trends have also been seen in menstrual care, with standard towels continuing to lose share to slim/thin/ultra-thin towels in 2024. As people are spending more time outside the home, demand for lighter, less bulky towels has surged. Slimmer towels with a minimalistic design are convenient for various activities and provide a comfortable feel. An increasing number of consumers are therefore switching to slim/thin/ultra-thin towels for daytime use, while continuing to use standard towels at night for extra protection.

The “2024 Problem” refers to challenges within the logistics industry due to stricter regulations on overtime for truck drivers, which took effect from April 2024. This reform is aimed at improving the historically long working hours of truck drivers by imposing limits on overtime. However, the logistics industry was already grappling with a severe shortage of drivers, exacerbated by an ageing workforce and a lack of younger recruits. In addition, the low wages relative to the demanding long-distance and long-hour work have further intensified the labour shortage. With the new labour regulations, companies now face the task of managing the same volume of work within reduced hours, While the intention behind the reform is positive, it highlights structural issues, which are creating significant challenges. Since April 2024, there have already been reports of increased transportation costs, rising prices for goods in stores, and delays in deliveries. Concern remains that the flow of goods will be disrupted, and various industries are struggling to implement effective countermeasures, which do not address the root causes of the problem. Consumers are beginning to feel the impact on their daily lives.

In response to these challenges, companies such as P&G Japan and Daio Paper are implementing innovative strategies to adapt to the 2024 Problem. P&G has leveraged an AI demand forecasting system to accurately predict demand at individual retail locations, optimising truck allocation and stabilising load capacities. It is also collaborating with retailers for joint deliveries to enhance transport efficiency. Meanwhile, Daio Paper is turning to the use of autonomous trucks to improve logistics efficiency, driven by the dual pressures of driver shortages and rising logistics costs. It is also promoting collaborative delivery efforts with both industry peers and companies from other industries, seeking solutions to the ongoing challenges posed by the evolving landscape of logistics and supply chain management.

Retail developments

Health and beauty specialists remained the dominant distribution channel within overall tissue and hygiene in Japan in 2024, with a stable share of sales. Intensifying competition is being seen in this highly competitive channel. Since the merger of Matsumotokiyoshi Holdings Co. and Cocokara Fine in 2021, forming MatsukiyoCocokara & Co., the expanded store network has not only provided greater reach, but has also enhanced the development and competitiveness of private label products. This has resulted in a high brand penetration rate amongst consumers and sustained price competitiveness. To further differentiate itself from other drugstores, it has created experience spaces focused on health and beauty, as well as offering various services to strengthen customer loyalty. In addition, investments in marketing strategies and digitalisation have contributed to maintaining its competitive edge.

Meanwhile, in 2024 Sugi Holdings Co. acquired the pharmacy I&H, while Tsuruha Co. and Welcia Holdings Co. announced plans for a merger, aiming for 2025. Sugi’s acquisition of I&H aims to strengthen its pharmacy business and leverage synergy effects for revenue growth, setting it apart from competitors. This move is expected to enhance its presence in the industry by surpassing Sundrug Co. in terms of scale. On the other hand, the merger between Tsuruha and Welcia is designed to pursue economies of scale, enhance logistics and purchasing power, and reduce costs, establishing a competitive advantage in the overall retail industry.

These developments are likely to further accelerate the mergers and integrations that have been ongoing within the industry, exacerbating the competitive environment within drugstores, which serves as the most critical channel in tissue and hygiene in Japan. As companies adapt and evolve, the landscape will become increasingly challenging. Historically, consolidation has been pursued for expansion and synergies, but distinct strategies and innovative approaches will be essential to maintain competitiveness in the future.

However, the most dynamic distribution channel in tissue and hygiene in 2024 for yet another year was retail e-commerce. Tissue products are bulky but low-priced, which means many e-commerce platforms price their products high, as they are not keen to sell and deliver such products. Nevertheless, retail adult incontinence and nappies/diapers/pants had relatively high shares of sales via retail e-commerce in 2024. This shows that when the situation is right, for instance when consumers value the discretion or convenience of home delivery, they may choose to buy online, despite drugstores usually having a lower price tag.

What next for tissue and hygiene?

Both retail and AfH tissue and hygiene are expected to continue growing in Japan in the forecast period in current value terms. However, some categories are anticipated to struggle to achieve volume growth. According to Euromonitor’s Consumers data, Japan’s population is projected to decrease by 3% from 2024 to 2029, with a further decline of 6% expected over the next decade. This demographic trend is exacerbated by a conservative culture that prioritises marriage before having children, coupled with a notable reduction in marriages, which fell by over 20% between 2019 and 2024, therefore limiting the birth rate. The Japanese government has reported that 2024 will see the lowest number of births and total fertility rate since records began in 1899. The decline, worsened by the pandemic, shows no signs of rebounding even as the effects of Covid-19 disappear. In fact, the number of births, which surpassed one million in 2014, is projected to drop below 700,000 in 2024. Categories such as retail tissue and menstrual care are expected to see volume decline due to the overall population decline. Meanwhile, nappies/diapers/pants is specifically expected to be impacted by the falling birth rate.

Meanwhile, Japan continues to experience significant ageing of its population. The proportion of individuals aged 65+ has risen from less than 20% in 2004 to over 29% in 2024. In addition, the population aged 75+ increased from 9% to 17% during the same period. Euromonitor’s data indicate that this trend will continue, with the number of people aged 65+ expected to increase both in absolute terms and as a percentage of the total population until 2029. The population aged 75 and over is also projected to grow by 8% during this time. This trend is anticipated to drive continued growth for both retail and AfH adult incontinence in the forecast period. These demographic shifts towards population decline, a low birth rate, and an ageing society, combined with ongoing price increases and a focus on high value-added products, are therefore expected to reshape the tissue and hygiene industry.

In response to these trends, companies are looking towards the growth of business-to-business (B2B) sales.

Given Japan’s ageing population, solutions tailored for the care of older people are anticipated to exhibit high growth potential.

Meanwhile, the continued influx of inbound tourists is expected to drive substantial demand for AfH tissue and hygiene. As tourism flourishes, the demand for high-quality tissue products will also rise, which will encourage companies to innovate and enhance their product lines.

Executive Summary

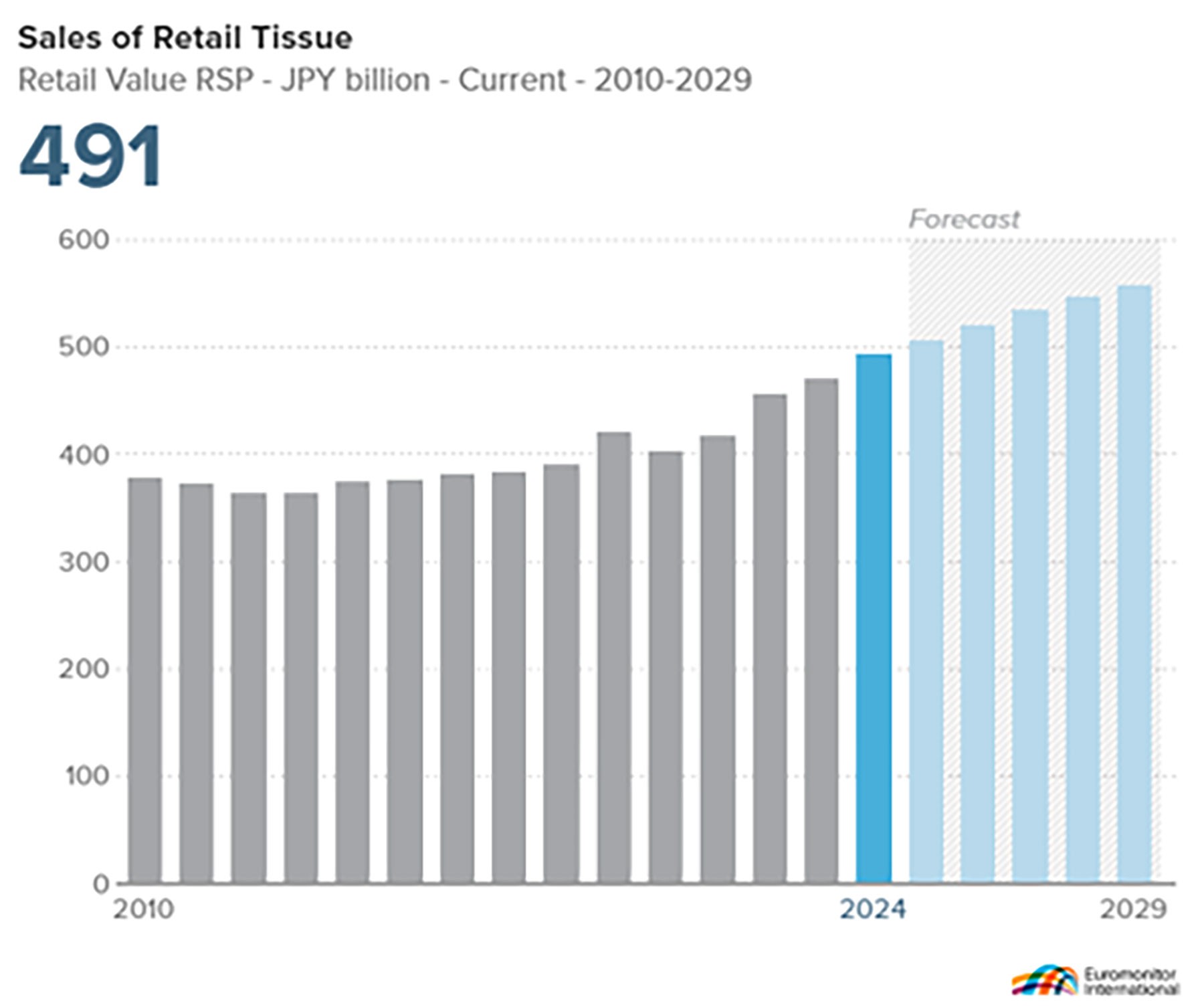

Retail value sales grow by 5% in current terms in 2024 to JPY491bn

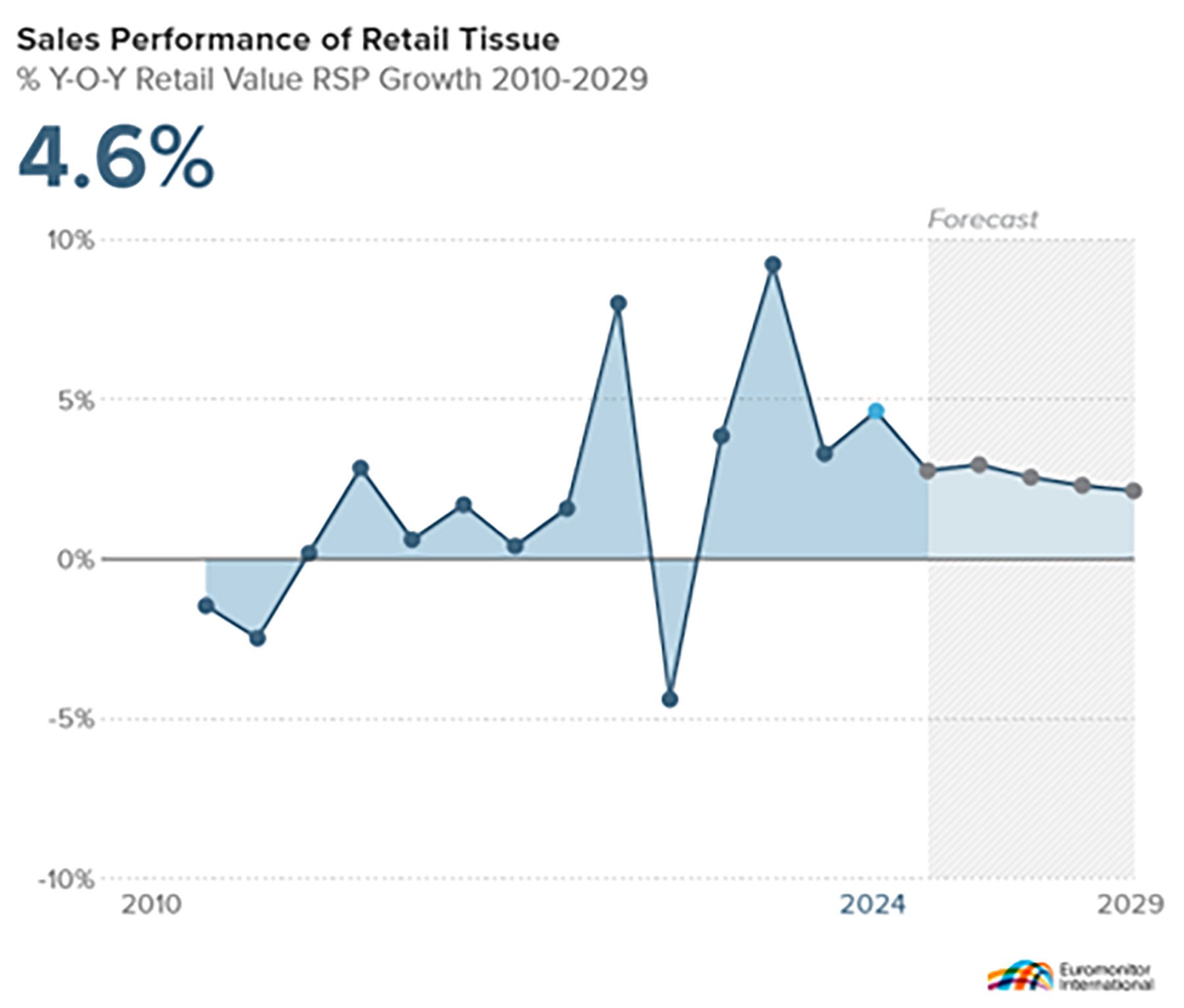

Facial tissues is the best performing category in 2024, with retail value sales increasing by 7% in current terms to JPY207bn

Retail sales are set to increase at a current value CAGR of 3% (2024 constant value CAGR of 1%) over the forecast period to JPY557bn

2024 Developments

Adapting to inflation with a focus on quality and innovation

Retail tissue in Japan continued its downward trend in retail volume terms in 2024, influenced by factors such as population decline, reduced time spent at home, and lower pollen levels compared with 2023. Nevertheless, sales increased in retail current value terms. Over the last three decades, Japan experienced relatively stable inflation rates, with a few exceptions. However, in 2022 inflation rose by 2.5%, followed by 3.3% in 2023, and another increase of over 2% in 2024. This marked a notable shift, as Japan faced continuous inflation for the first time in 30 years. Despite previous concerns that price increases could lead to a loss in market share, companies had to undertake measures to raise prices and reduce product sizes, resulting in solid value growth.

Retail tissue products are particularly sensitive to promotional campaigns from manufacturers and retailers. However, despite ongoing inflation in 2024, consumers did not immediately shift to cheaper product lines or private label lines. Even as societal behaviours returned to pre-pandemic norms, there remained a heightened awareness of infectious diseases, such as influenza, which meant that consumers moved towards valuing quality over quantity where possible, and this drove value growth for essential hygiene products such as toilet paper and facial tissues, with the latter seeing the strongest value growth in 2024. Consumers also continued to choose higher-priced products that emphasised convenience and softness, especially in the largest category, toilet paper. For example, in July 2024 Oji Nepia launched a new toilet roll under the Nepia brand, Karada Omoino Toilet Roll, literally meaning “toilet roll caring for the body”, featuring four layers with 1.5 times the absorbency of traditional products. This innovation reduces friction and incorporates a silky touch finish which is gentle on sensitive skin, demonstrating the potential for high-value products to maintain share amidst economic challenges.

Prospects and opportunities

Demand for premium products set to grow despite demographic decline

Retail tissue in Japan has reached a mature stage, and with long-term population decline likely to be unavoidable, retail volume sales are expected to continue to fall. According to Euromonitor’s Consumers data, Japan’s total population is projected to decrease by 3% from 2024 to 2029, with an estimated decline of 6% over the next decade. Coupled with the conservative cultural norm of having children only after marriage, and a decrease of over 20% in marriages from 2019 to 2024, the outlook for population growth appears bleak.

Nevertheless, retail current value sales are anticipated to continue to rise. Despite the challenges, there is a notable trend towards higher value retail tissue products, such as those with a gentle touch and added fragrance. In addition, events such as the Noto Peninsula earthquake in January 2024 have heightened awareness of the need for disaster preparedness, leading to increased demand for stockpiling essential items such as toilet paper. The Ministry of Economy, Trade and Industry has also been active in promoting household stockpiling of toilet paper, which suggests steady value demand.

Looking ahead to 2025, both Daio Paper and Oji Nepia have announced plans to revise manufacturer shipment prices for retail tissue products, including tissue paper, toilet paper, and kitchen towels, by more than 10%. This indicates a continuation of the upward trend in product pricing, driven by the need to adapt to the changing market conditions. While the overall category may face challenges achieving volume growth due to demographic shifts, the demand for high-value, essential products is expected to remain robust. Although toilet paper is expected to remain the largest category, pocket handkerchiefs expected to see particularly strong growth from a low base.

Educational initiatives to build brand loyalty

As the domestic market faces a long-term decline in demand for retail tissue products due to the decreasing birth rate and the shrinking population, Oji Nepia has taken proactive steps to enhance brand recognition and secure its future customer base through educational initiatives. These awareness programmes not only assist consumers in understanding the appropriate use of products and fostering healthy lifestyle habits but also contribute to building a loyal customer foundation and increasing brand visibility. Furthermore, through its social contribution activities, the company aims to enhance its corporate image while pursuing sustainable growth.

In August 2024, Oji Nepia, in collaboration with the non-profit organisation Japan Toilet Labo, relaunched its Unchi Kyoushitsu (Poop Classroom) programme after five years – with the last time it was run being before the pandemic outbreak. This initiative focuses on teaching children the importance of bowel health in a fun and engaging way, whilst also promoting awareness of environmental considerations associated with toilet paper usage. Through these efforts, Oji Nepia is committed to nurturing the next generation of consumers and reinforcing the relevance of its brand in a changing market.